How Stakeholder Tensions Impact Acquirer’s Managerial Overcommitment and Synergy Destruction in M&A Transactions

Mergers and Acquisitions (M&A) are an important source of external growth and corporate development. Even though recent research from Bain & Company shows that due to improved practices, 70% of mergers succeed, research still reports that acquisitions on average fail to create any value.

1. Introduction

Mergers and Acquisitions (M&A) are an important source of external growth and corporate development.1 Even though recent research from Bain & Company shows that due to improved practices, 70% of mergers succeed2, research still reports that acquisitions on average fail to create any value.3 Despite potential improvements, “big one-off deals remain risky”, where mergers that grabbed headlines end up failing.4

This raises why mega-deals still face a 50-50 success chance despite recent gains, as McKinsey notes firms using large-deal strategies are no more likely to outperform peers.5 This raises why mega-deals still face a 50-50 success chance despite recent gains, as McKinsey notes firms using large deal strategies are no more likely to outperform industry peers.6 The sheer value of these deals makes it important to understand why those mega-deals are riskier. While most strategy researches are based on the success factors, making it difficult for practitioners to “learn from failure”, this article focuses on the reasons for failure.

Notably, M&A transactions often involve complex relationships between stakeholders, especially in mega-deals, where decisions by acquirers or sellers could trigger negative reactions of multiple stakeholders depending on their interests. While such reactions are logical responses for self-preservation, they could disrupt the acquisition process and ultimately destroy the value potential. This research, therefore, examines how stakeholder tension impacts acquisitions by using the Bayer-Monsanto acquisition, the second-largest deal in Germany‘s transaction history, which faced widespread controversy over its strategic rationale and industry impact.7

2. Stakeholder influence and tensions in M&A transactions

In M&A, one major stakeholder tension typically occurs between the acquirer and seller, particularly around pricing, payment structure, and other deal terms from negotiation before deal closing. These tensions are significantly shaped by the relative bargaining power of each party, impacted by the deal process, management’s experience and firm characteristics.

Bargaining power can differ depending on the acquisition process, where the seller‘s power is stronger in competitive bidding compared to dyadic processes, which commonly increases the speed and commitment of acquirers during negotiations.8,9 Information asymmetry on both sides also impacts each other’s bargaining power, as both sellers and buyers mutually assess the synergic potential of the acquisition, where more information becomes a crucial factor for evaluating acquisition synergies.10,11,12 Typically, buyers are faced with greater information asymmetry compared to the target, especially if the deal is hostile, the target’s industry is diverse and differs from the acquirer’s primary business, or it is private and is not subject to scrutiny and disclosure requirements.13,14,15 Research shows that acquirers’ weak bargaining power with high information asymmetry, added to bidding competition, could result in escalating commitment of acquirers towards the target, fuelled by managerial self-interest, overconfidence and risk propensity, disregarding negative or unfavourable information.16

Looking into experiences, prior experience plays a large role in dealing with high information asymmetry situations.17 Prior acquisition experience contributes to improved negotiation skills due to adaptive learning, developing a more accurate representation of their opponent’s behaviour, priorities and alternatives, or capturing more value compared to inexperienced counterparts.18 However, experience might also trigger the illusion of control, where superstitious learning and an oversimplified view towards potential targets lead to target assessment failure.19,20,21 Often, acquirers have distinct, limited perspectives influenced by the senior managers’ functional backgrounds, their dominant coalition, powerful suppliers, customers, and financiers, which limit their consideration of the target and ultimately harm their judgment.22

Besides, different stakeholders‘ interests could impact the deal directly and indirectly. Before the deal announcement or exposure of the transaction to the public, the number of stakeholders involved is limited, with M&A advisors often becoming the most influential third party in shaping the direction and structure of the deal alongside the buyer and seller. Their contributions are mainly around reducing transaction costs and strengthening bargaining power by facilitating the negotiation/bidding process, minimising information asymmetry, and mitigating contracting costs.23 Nevertheless, M&A advisors might be affected by cognitive biases and heuristics due to a lack of information, time constraints, standardisation of the search process, and emotions.24,25 This could lead to the ignorance of potential targets, and especially organisational fit between the entities, as they are difficult to measure.26 Moreover, their motivation could solely come from fees, which creates agency problems, making them focus on deal closure rather than considering value creation after the acquisition, pushing clients into unnecessary deals.27,28,29

Other important stakeholders include regulators, shareholders, and the public, who could also impact the direction or outcome of an acquisition deal by colliding with their interests.30,31 These tensions mainly arise when the deal becomes publicly exposed during negotiation, offer, or the deal announcement, as it allows various stakeholders to begin responding based on their perceived gains and losses.32 For instance, shareholders and regulators could directly impact the execution of the deal, as shareholders’ support is essential for deal approval, and regulators hold the legal authority to authorise or block deals, directly shaping feasibility and timing. Although not directly influencing deal closure, tensions from the public, such as environmentalists, consumer groups, or politicians, could indirectly impact the deal’s outcome through pressuring regulators, the public image of the deal or the firm, resulting in negative market reaction or a drop in sales.

Importantly, these stakeholder tensions do not arise in isolation; it is the interaction of multiple stakeholder tensions that could combine and trigger managerial overcommitment, potentially resulting in the sunk-cost fallacy. This article is trying to disentangle the complexity and effects of stakeholder tensions through analysing the Bayer-Monsanto deal. In other words, this article will illustrate how stakeholder tensions arose during the deal and how they pressured management to make ill-informed decisions, resulting in overpayment and synergy destruction.

3. Bayer and Monsanto Acquisition Case: Escalating commitment and synergy destruction

3.1. Background of Bayer-Monsanto deal

Agriculture used to be an industry resistant to accumulation due to unpredictable risks of weather, pests and the perishable nature of food.33 However, technological development post-World War II enabled economies of scale for agricultural products through upgraded hybrid seeds, pesticides, and fertilisers, leading to lower prices.34 This enabled capital accumulation in the industry, which shifted from a sector characterised by multiple smaller players into an industry dominated by a small number of transnational pharmaceutical/chemical corporations.35

Followed by horizontal acquisitions, acquisition strategies have extended vertically and globally to own both traits and seed patents, covering the whole supply chain.36,37 In 2015, Syngenta accepted the offer of ChemChina, and in 2016, DuPont and Dow announced their merger.38,39

Following this trend, Bayer, incorporated in Germany, acquired Monsanto, based in the US, in 2018. Bayer is a biochemical company active in four areas: pharmaceuticals, consumer health, agriculture (“Bayer Crop Science”), and animal health.40 Internal accounts show that Bayer wanted to conduct long-term investments in their crop science division, considering the increasing global population and therefore gain back market share from the other two major competitors. For Bayer, Monsanto was a strong target as they were the leading company in the seed business, where Bayer had a weaker presence.41

Manager A: “Of course, this was driven by the business development of Bayer, so they had an idea to conduct a long-term investment in their crop science business. And the major reason for that was market share, and they were not the largest company in that regard…they (Bayer) were attracted to Monsanto because Monsanto was also very advanced in this (seed business)…”

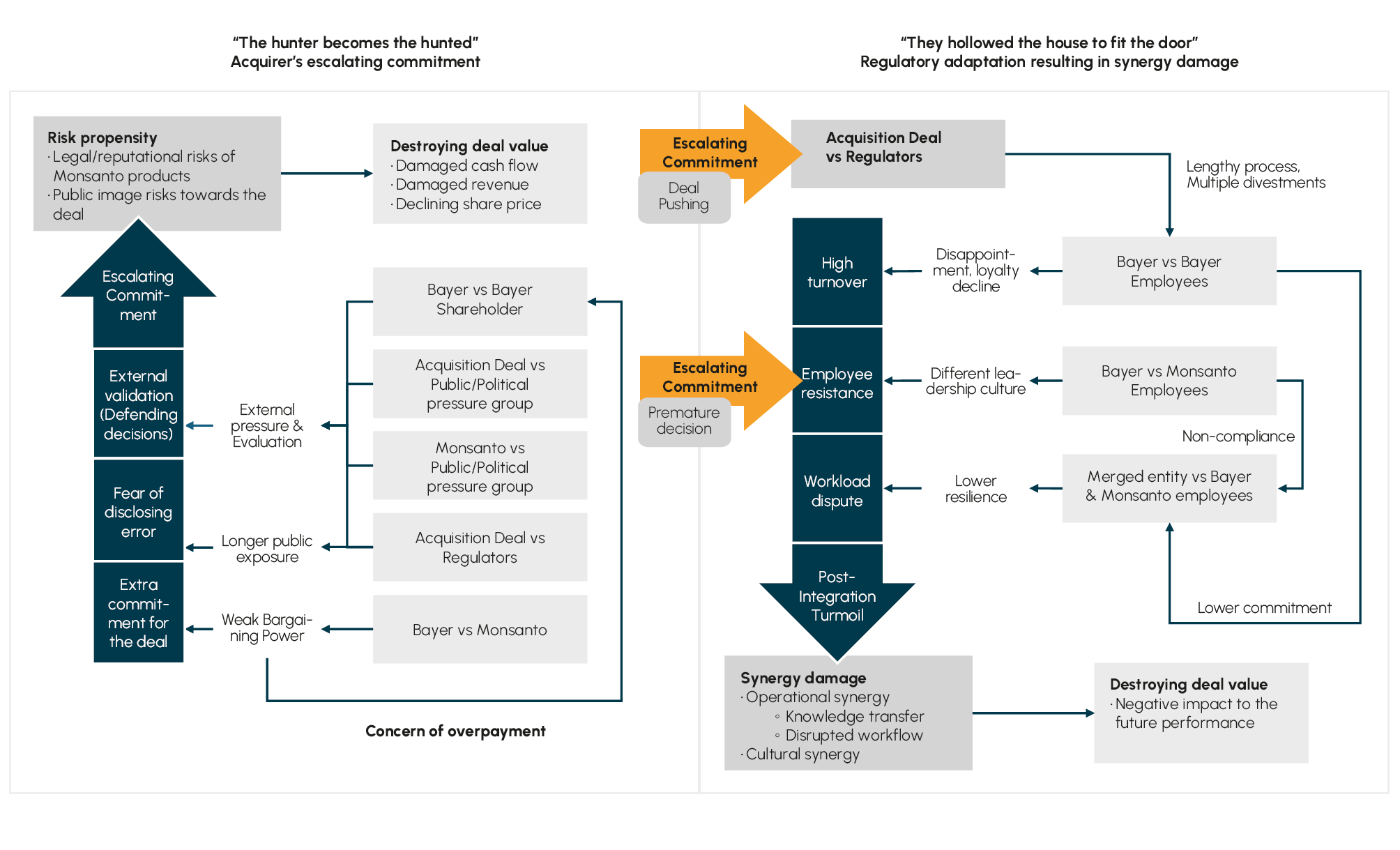

3.2. Bayer’s escalating commitment and risk propensity

From the first offer in May 2016, pricing disagreements created tensions between Bayer and Monsanto, with Monsanto rejecting multiple offers.42 Due to few alternatives in the agrochemical industry and Monsanto’s attractiveness as a target, Bayer inevitably started from a position with relatively weak bargaining power, despite sufficient information availability due to Monsanto’s public profile and Bayer’s domain expertise.

Manager A: “From a buyer‘s perspective, when you don‘t have a lot of alternatives, you want to have this deal that gives you a weaker position in negotiating because you are desperate, you know. So it‘s depending on your alternatives… ”

Such tension likely contributed to the escalation of Bayer’s commitment, where Bayer’s management pushed the deal by increasing the acquisition price from $122 to $128 per share, signing the agreement in September 2016.43 Research has shown that strong seller bargaining power can accelerate both the speed and commitment of acquirers during the transaction process.44,45

However, in the Bayer case, regulatory pressures significantly prolonged the acquisition process. While both Bayer and Monsanto anticipated scrutiny, as shown in a $3bn break-up fee, they did not expect the depth and intensity of investigation, such as the focus on innovative competition and a lengthy approval timeline from the EU and U.S DoJ, lasting until 2018.46,47,48

Manager A: “….authorities…. they blocked the deal for many, many months, and it wasn‘t expected like that. Usually, when you have (deal) announcement, in an ideal case, within four to six weeks, you close the deal. But that wasn‘t the case.”

Manager A: “…the tricky part was that, usually, the authorities, they‘re looking at the revenue and they‘re looking at the competition…That is usually the case, and they did that. But on top of it, they looked at the intellectual property Bayer and Monsanto has. And they compared this intellectual property with the intellectual property of other companies. This is new….and nobody expected that came up in the first time here…We had even somebody from the European Commission as a permanent observer in the deal… There were four or five times they changed and extended the scope more and more…”

Given the oligopolistic nature of the industry and antitrust concerns, such delays and public exposure of the deal were largely inevitable. Nevertheless, Bayer’s management pushed to close the deal for nearly 2 years after the deal announcement, ultimately resulting in divesting a significant amount of assets to BASF, amounting to €7.4bn.49,50 Despite regulatory delays and divestment-related concerns, Bayer’s CEO continued to publicly defend the Monsanto acquisition throughout the approval process. At the AGM in May 2018, after the EU regulatory clearance, he defended delays and regulatory reviews of the deal by emphasising the potential of long-term value to shareholders, despite the expected $300m loss in synergy stemming from divestments.51,52

Werner Baumann, CEO of Bayer AG: “I‘m convinced that this acquisition has very great potential for creating value for our company, our stockholders and our customers.”53

Following the deal’s closure in June 2018, despite lower expected earnings and legal claims from Monsanto’s products, he reinforced his position.54

Werner Baumann, CEO of Bayer AG: “The Monsanto business is very healthy… we are as excited as we have ever been about the combination, and there are absolutely no regrets.”55

The CEO’s continued public defence of the deal reflects a classic escalation pattern, where leaders under scrutiny seek to justify their prior decision. Studies show that such commitment prevails more when their actions are under public observation, to avoid losing credibility and exposing errors.56 While some research suggests that regulations can moderate it57, others indicate that external threats often encourage such commitment to rationalise flawed decisions.

58,59In Bayer’s case, the CEO’s push for the deal closure and the rationalisation of their action, despite the legal and regulatory scrutiny, shows an escalation of commitment aimed at defending their earlier decisions and avoiding exposing errors, rather than reconsidering the deal under external pressure.

This perspective also extends beyond regulatory scrutiny; public pressures could similarly fuel escalating commitment. After the first offer was publicly disclosed, public opinions, consumer groups, public interest groups, and politicians opposed the deal with similar concerns. These concerns centred on the concentration of the agricultural input market and the disruption of the sustainable food supply chain by genetic engineering.60,61,62,63,64,65,66 Given the oligopolistic nature of the agrochemical industry and public fear of GM engineering, such tension was inevitable. This shared tension from the public and political pressures appeared to harm the public image of the deal through protests, petitions, and the voice of politicians.

Manager A: “…But that (protests) didn‘t have an impact on the deal itself. Usually, you have to deal with your investors. Best sorts are influenced by the public, so you need to also have a good communication to the public.”

Moreover, since the pre-acquisition period, conflicts between the public and political groups and Monsanto have existed regarding products such as glyphosate, causing cancer, exerting significant external pressure by reputational and legal risks to the deal.67,68,69,70 This spilt over to Bayer, as it was inherent in the very nature of Monsanto’s business. Ultimately, these pressures and evaluations likely further escalated Bayer’s commitment, similar to the regulatory pressure, deepening their level of commitment to defend their earlier decisions.

Shareholders’ concerns over the deal following the initial offer likely exerted pressure on management as well, given that managers act as agents of shareholders, who hold the authority to influence or replace them.71 However, unlike other tensions, this could have been avoided by strengthening Bayer’s bargaining position from the outset. Studies suggest that an acquirer could cover up their weak bargaining stance by low initial premium, low cash offers, or reducing time pressure through extending negotiations, thus avoiding escalating commitment.72 Instead, Bayer chose to push the deal by increasing the price, indicating that its management was not motivated to preserve its bargaining power. This decision ultimately heightened concerns among shareholders about the risk of overpaying for Monsanto, leading to a strong tension with Bayer’s management.

Manager A: “I think Bayer was questioned from the market if they could afford such a big deal…”

Paradoxically, this shareholder pressure, rather than prompting reassessment, appeared to encourage Bayer’s managers to seek external validation to defend decisions by convincing shareholders of the deal’s long-term value, reinforcing its commitment to the deal closure.73

Manager A: “…and they (Bayer) always argued with a long-term strategy, and for this reason, it got approved. Bayer could convince the shareholders that long-term value was increasing dramatically compared to if the deal wouldn‘t have happened…”

By pushing the deal, Bayer’s management successfully closed it in June 2018, despite regulatory, public image, and target-related risks through significant divestments. However, this early escalation commitment contributed to a greater risk propensity. Manager A mentioned that Monsanto’s legal risk “was not underestimated” by Bayer’s lawyers, as they “knew exactly what they were dealing with” regarding the US legal system. Indeed, Bayer “validated and calculated” those risks into the deal, where everybody insisted on waiting until the lawsuits were settled. However, Manager A added that “the CEO and part of the management team really wanted to get this through”, where they were “insisting on this deal not losing face”, making decisions “personal” instead of “rational”, at the same time, “ignoring the signs”. Prior research shows that escalating commitment of acquirers towards the target, fuelled by managerial overconfidence and risk propensity, disregards negative or unfavourable information.74,75 Thus, this illustrates Bayer’s management’s risk tolerance and overconfidence regarding Monsanto’s legal and reputational risks through a higher commitment to proceed with the deal.

Eventually, these accumulated risks from stakeholder tensions, which Bayer did not manage properly, haunted the company back. Due to Monsanto’s product issues, Bayer faced 125,000 lawsuits, draining cash flow and revenue by paying up to $10.9 bn to settle roughly 100,000 Roundup cases.76,77 Product bans also occurred in multiple European countries, where France banned some of the Roundup products.78 Germany, Italy, and Austria also restricted the use of glyphosate, leading to revenue loss.79,80,81 Ultimately, this further pressured the tension between Bayer and shareholders during the post-acquisition period by dropping share price, resulting in shareholder activism with a no-confidence vote towards management in 2019.82

Taken together, the findings show how multiple layers of stakeholder tension: Bayer’s weaker bargaining power with Monsanto; prolonged public exposure of decision-making due to the extended regulatory process; mounting external pressure from the regulators, shareholders, and public groups; collectively drove management to escalate commitment to Monsanto. This escalation ultimately led to failures in risk management and a negative outcome.

3.3. Impact of escalating commitment to employee-related risks and synergy destruction

Beyond shareholder dissatisfaction, escalating commitment also had lasting consequences for Bayer’s internal stakeholders, particularly its employees, undermining the integration process and cultural/operational synergies. Internal accounts suggest that there were tensions between the deal and Bayer employees stemming from multiple divestments and a lengthy process, with high turnover (“losing people”) (Manager A) and “disappointment” among divested employees (Manager B).

However, the divestments were unavoidable for successful deal closure, given the regulatory challenges surrounding the deal. At this stage, Bayer could have reconsidered the acquisition during this period, considering the impact of divestments on the company. Instead, as mentioned in 3.2, Bayer pushed the deal, driven by escalating commitment. As a result, the consequences of regulatory delay and employee fallout become embedded in the deal’s execution.

Research confirms that uncertainties during the merger phase can reduce organisational commitment and lead to high turnover.83,84 Moreover, divestments often violate employees’ psychological contracts with the firm, weakening their sense of loyalty, leading to lower commitment and lower tenure.85,86,87 Manager B also noted that Bayer’s employees had a strong attachment to the company, where “employees have grown up with Bayer in Leverkusen and (their) identity is Bayer”.

Indeed, this deep connection suggests that divestments, compounded by lengthy regulatory approval, eroded strong loyalty and heightened uncertainty among employees, likely triggering knowledge loss via high turnover, undermining post-deal operational synergies.88,89 Thus, even if unintended, Bayer’s commitment to closing the deal at all costs intensified regulatory and employee-related tensions, adversely affecting its relationship with employees and likely weakening its internal capacity to integrate and transfer organisational knowledge.

Moreover, internal accounts illustrate that there was a cultural clash between Bayer and Monsanto employees. Although this tension may seem unavoidable given that Monsanto’s distinct leadership style was beyond Bayer’s control, Bayer’s management made this matter worse by blending the leadership positions with Monsanto.

Manager B: “… So you have two organisations, you have the Bayer and the new Monsanto, and you would say this one (Monsanto) goes exactly underneath, but you need to integrate the culture, and somehow the leadership team then mixed up... and so some of the Bayer leaders lost their job over, downgraded in such a sense”

Manager B: “… with the integration of the culture, it might not be a good fit sometimes… The culture was completely, was maybe a crash and did not fit so easily to each other because there were different leadership styles.”

Given that the cultural differences mainly stemmed from the contrasting leadership styles, integration measures likely created further organisational confusion. This reflects what has been described as a ‘premature solution’, where escalating momentum’s desire to complete the deal quickly overrides deeper considerations of organisational and strategic fit.90 As a result, due diligence on organisational compatibility was likely deprioritised, undermining the cultural synergy by hindering the establishment of a unified corporate identity.91

Ultimately, escalating commitment appeared to have facilitated both employee-related tensions from regulatory pressure and a cultural clash. These tensions likely manifested in the tension between the merged entity and its employees. Internal accounts show that employees had a dispute over the post-integration workload.

Manager B: “Another element is that you have new processes, (there are) new tools in place that you need to integrate… not everyone loves to do the integration work because that‘s a lot of work and you need to integrate a new organisation… I think that can be mentioned as well as a dispute between the people and maybe the organisation.”

This suggests that reduced organisational commitments of employees, driven by earlier disappointment and uncertainty from regulatory pressure, may have undermined their resilience to the increased workload during the integration phase. Research shows a strong link between organisational commitment and resilience, with emotional commitment playing a critical role.92 In Bayer’s case, employees diminished attachment and resulting disappointment likely eroded resilience, disrupting workflows and thereby harming the realisation of operational synergy.93

In addition to these commitment-related issues, cultural differences further exacerbated the situation. Studies show that cultural clashes can trigger distrust, hostility and self-preservation, and non-compliance with integration processes.94,95,96 In this context, Bayer’s cultural integration challenges, intensified by management’s premature decision, likely disrupted workflows as well via non-compliances and hostility.

Taken together, these dynamics illustrate how escalating commitment deepened employee-related tensions and cultural clashes. The combined effect of reduced commitment and cultural resistance critically undermined resilience, ultimately harming post-deal operational performance.

Fig. 1 Summary of Acquirer’s escalating commitment and its impact on the Bayer-Monsanto deal

Quelle: Own illustration

4. Conclusion and implications

To sum up, this article shows that stakeholder tensions can trigger managers’ escalating commitment. Bayer’s weaker bargaining power stemming from the tension with Monsanto encouraged managers’ increased commitment. An extended public exposure due to regulatory tension heightened the fear of error disclosure, further reinforcing this commitment. Pressures from regulators, shareholders, and public/political groups created a need for external validation, prompting management to continuously defend their strategic choice, thus increasing their commitment.

Notably, instead of addressing their weaker bargaining position during the offer phase, which could have reduced escalating commitment, management increased the acquisition price to push the deal forward. Ironically, this decision exacerbated shareholder tensions over potential overpayment, and the resulting pressure further intensified management’s need for external justification, ultimately reinforcing the very commitment that caused the tension in the first place. Ultimately, risk propensity from escalating commitment of management led to an underestimation of accumulated legal, reputational, and public image risks from multiple stakeholder tensions, destroying deal value during integration with product bans and lawsuits.

Besides, this article illustrates how escalating commitment amplifies employee-related tensions by embedding regulatory force and prompting premature decisions in cultural integration. The CEO and management’s willingness to push the deal to closing, fuelled by escalating commitment, made multiple divestments and lengthy investigations from regulators inevitable. This created disappointment and uncertainty among employees, lowering the commitment and leading to high turnover, damaging operational synergy by disrupting knowledge transfer.

Escalating commitment also led to the flawed post-integration decision of blending top management between Bayer and Monsanto, despite significant differences in leadership culture. This move neglected considerations of organisational fit and resulted in a “premature” solution that further intensified the cultural conflict between Bayer and Monsanto employees, leading to stronger resistance towards the post-acquisition. This undermined cultural synergy by disrupting cultural unification. Eventually, the resulting lower commitment and non-compliance from both tensions potentially intensified tensions over the post-integration workload dispute via declining resilience, further harming the realisation of operational synergy.

Overall, effectively managing escalating commitment bias could have helped Bayer reduce overpayment, shareholder conflicts, poor risk management, and employee-related risks. Accordingly, if the firm (as an acquirer) is inevitably in a weaker bargaining position, managers are recommended to strengthen bargaining power by extending the negotiation timeframe with a lower premium. This would help prevent managers from making flawed decisions such as overpayment, thereby reducing the tendency to escalate commitment from rationalising errors. Minimising the tendency to escalate commitment and strengthening bargaining power would assist in alleviating shareholder concerns and improving risk management by avoiding overpayment and ensuring thorough due diligence. Although regulatory pressure, public scrutiny, and deal exposure may still be unavoidable in mega-deals, reducing this bias from the outset would help managers avoid “locking in” a decision and encourage consideration of alternative strategies such as joint ventures and strategic partnerships, which could reduce risks of employee-related tensions during integrations.

1 Bauer/Matzler, Antecedents of M&A success: The role of strategic complementarity, cultural fit, and degree and speed of integration, Strategic Management Journal, Vol. 35, No. 2, 2014, pp. 269–291.

2 Harding/Stafford/Kumar, How Companies Got So Good at M&A, Bain & Company, 2024, online: https://www.bain.com/insights/how-companies-got-so-good-at-m-and-a/.

3 King/Wang/Samimi/Cortes, A Meta-Analytic Integration of Acquisition Performance Prediction, Journal of Management Studies, Vol. 58, No. 5, 2021, online: https://doi.org/10.1111/joms.12636

4 See note 2

5 Daume/Lundberg/Montag/Rudnicki, The flip side of large M&A deals, McKinsey & Company, 2022, online: https://www.mckinsey.com/capabilities/m-and-a/our-insights/the-flip-side-of-large-m-and-a-deals

6 Ibid

7 Statista, Largest merger and acquisition (M&A) deals in Germany as of May 2024, by deal value, Statista, 2024, online: https://www.statista.com/statistics/410886/biggest-manda-transactions-germany/

8 Dreher/Ernst, Mergers & Acquisitions: Understanding M&A Processes for Large- and Medium-Sized Companies, Springer Nature Switzerland AG, 2022.

9 Welch/Pavićević/Keil/Laamanen, The Pre-Deal Phase of Mergers and Acquisitions: A Review and Research Agenda, Journal of Management, Vol. 46, No. 6, 2020, online: https://doi.org/10.1177/0149206319886908

10 Luypaert/Van-Caneghem, Exploring the Double-Sided Effect of Information Asymmetry and Uncertainty in Mergers and Acquisitions, Financial Management, Vol. 46, No. 4, 2017, p. 873–917, online: https://doi.org/10.1111/fima.12170

11 Graebner/Eisenhardt, The seller’s side of the story: Acquisition as courtship and governance as syndicate in entrepreneurial firms, Administrative Science Quarterly, Vol. 49, No. 3, 2004, p. 366–403.

12 See note 9

13 Graebner/Eisenhardt/Roundy, Success and failure in technology acquisitions: Lessons for buyers and sellers, Academy of management perspectives, Vol. 24, No.3, 2010, p. 73-92. doi:https://doi.org/10.1016/j.jebo.2006.04.003.

14 Reuer/Ragozzino, Adverse selection and M&A design: The roles of alliances and IPOs, Journal of Economic Behavior & Organization, Vol. 66, No. 2, 2008, p.195–212.

15 Cuypers/Cuypers/Martin, When the target may know better: Effects of experience and information asymmetries on value from mergers and acquisitions, Strategic Management Journal, Vol. 38, No. 3, 2016, p.609–625. doi:https://doi.org/10.1002/smj.2502.

16 See note 9

17 See note 15

18 Ibid

19 Aschbacher/Kroon, Falling Prey to Bias? The Influence of Advisors on the Manifestation of Cognitive Biases in the Pre-M&A Phase of Organizations, Group & Organization Management, Vol. 50, No. 1, 2023, p.41-81. doi:https://doi.org/10.1177/10596011231171455.

20 Duhaime/Schwenk, Conjectures on Cognitive Simplification in Acquisition and Divestment Decision Making, The Academy of Management Review, Vol. 10, No. 2,1985, p.287. doi:https://doi.org/10.2307/257970.

21 Zollo, Superstitious Learning with Rare Strategic Decisions: Theory and Evidence from Corporate Acquisitions, Organization Science, Vol. 20, No. 5, 2009, pp.894–908. doi:https://doi.org/10.1287/orsc.1090.0459.

22 Jemison/Sitkin, Corporate Acquisitions: A Process Perspective. The Academy of Management Review, Vol. 11, No. 1,1986, p.145. doi:https://doi.org/10.2307/258337.

23 Davidson III/Tong/Proctor, Why bidding firms do not hire financial advisors in Mergers and Acquisitions, Corporate Ownership and Control, Vol. 5, No. 3, 2008, doi:https://doi.org/10.22495/cocv5i3c2p7.

24 Bauer/Dao, Target screening: a key strategic success factor for acquisitions, A Research Agenda for Mergers and Acquisitions, 2024, p.41–64.

25 Santana/Nguyen/Mirc/Rouziès, Chapter 1: Heuristics in pre-merger processes, A Research Agenda for Mergers and Acquisitions, Edward Elgar Publishing, 2024. https://doi.org/10.4337/9781035319077.00010

26 Ibid

27 Benoliel, Hazards to Effective Due Diligence, Eurasian Journal of Business and Management, Vol. 3, No. 1, 2015, p.1–7. doi:https://doi.org/10.15604/ejbm.2015.03.01.001.

28 Servaes/Zenner, The Role of Investment Banks in Acquisitions, Review of Financial Studies, Vol. 9, No. 3, 1996 pp.787–815. doi:https://doi.org/10.1093/rfs/9.3.787.

29 Agrawal/Cooper/Lian/Wang, Common Advisers in Mergers and Acquisitions: Determinants and Consequences, The Journal of Law and Economics, Vol. 56, No. 3, 2013. pp.691–740.

30 Wong/O’Sullivan, The Determinants and Consequences of Abandoned Takeovers, Journal of Economic Surveys, Vol. 15, No. 2, p.145–186, 2001, doi:https://doi.org/10.1111/1467-6419.00135.

31 Koo, Stakeholders’ Influence on Mergers and Acquisitions: A Research Review and Complementary Research Design, Kobe International University Economics and Management Collection, Vol. 36, p.1–20, 2016.

32 See note 30

33 Howard, Visualizing Consolidation in the Global Seed Industry: 1996–2008, Sustainability, Vol. 1, No. 4, 2009, p.1266–1287. doi:https://doi.org/10.3390/su1041266.

34 Ibid

35 Ibid

36 Joseph, Innovation, Patents, and Competition in Modern Agriculture: A Case Study of Bayer and Monsanto Merger, The Antitrust Bulletin, Vol. 66, No. 2, 2021, p.214–224. doi:https://doi.org/10.1177/0003603x21997022.

37 See note 29

38 Ibid

39 Lianos/Katalevsky, Merger Activity in the Factors of Production Segments of the Food Value Chain: A Critical Assessment of the Bayer/Monsanto merger, Centre for Law, Economics and Society (CLES), Faculty of Laws (UCL), 2017.

40 See note 33

41 Ibid

42 Guardian, Monsanto rejects Bayer’s $62bn takeover bid, The Guardian, 2016, Available at: https://www.theguardian.com/business/2016/may/24/monsanto-rejects-bayers-62bn-takeover-bid-gm-crops-us-agribusiness

43 Davies, Bayer raises Monsanto cash takeover offer to $65bn, The Guardian, 2016, Available at: https://www.theguardian.com/business/2016/sep/06/bayer-raises-monsanto-cash-takeover-65bn-dollars.

44 See note 9

45 See note 8

46 Massoudi/Khan, Bayer closes in on $66bn deal with Monsanto, Financial Times, 2016, Available at: https://www.ft.com/content/37691718-7a05-11e6-97ae-647294649b28.

47 European Commission, Case M.8084 – BAYER / MONSANTO: MERGER PROCEDURE REGULATION (EC) 139/2004, European Commission, 2018, Available at: https://ec.europa.eu/competition/mergers/cases1/202150/M_8084_8063752_13335_9.pdf

48 Dye/Buck/Shubber, Bayer is cleared by DoJ for $66bn Monsanto takeover, Financial Times, 2018, Available at: https://www.ft.com/content/ad5bdc0a-6331-11e8-90c2-9563a0613e56

49 Toplensky, EU greenlights $66bn Bayer-Monsanto deal, Financial Times, 2018, Available at: https://www.ft.com/content/f9ee52ce-2cf3-11e8-9b4b-bc4b9f08f381

50 McGee, BASF unveils biggest acquisition in its history, Financial Times, 2017, Available at: https://www.ft.com/content/4b87a028-b007-11e7-aab9-abaa44b1e130

51 Neate, Monsanto to ditch its infamous name after sale to Bayer, The Guardian, 2018, Available at: https://www.theguardian.com/business/2018/jun/04/monsanto-to-ditch-its-infamous-name-after-sale-to-bayer.

52 Reuters, Bayer cuts Monsanto synergy target to $1.2 bn due to divestments, Reuters, 2018, Available at: https://www.reuters.com/article/business/bayer-cuts-monsanto-synergy-target-to-12-bln-due-to-divestments-idUSF9N1SA02K/.

53 Bayer, Bayer is making good progress strategically, Bayer, 2018, Available at: https://www.bayer.com/media/en-us/bayer-is-making-good-progress-strategically/.

54 Kresge/Loh, Bayer CEO Has ‘No Regrets’ for $63 Billion Monsanto Purchase, Bloomberg.com, 2018, Available at: https://www.bloomberg.com/news/articles/2018-09-05/bayer-sees-earnings-lower-after-63-billion-monsanto-purchase?embedded-checkout=true.

55 Ibid

56 Ross/Staw, Expo 86: An Escalation Prototype, Administrative Science Quarterly, Vol. 31, No. 2, 1986, p.274. doi:https://doi.org/10.2307/2392791.

57 Molden/Hui, Promoting De-Escalation of Commitment: A Regulatory-Focus Perspective on Sunk Costs, Psychological Science, Vol. 22, No. 1, 2011, p.8–12. doi:https://doi.org/10.1177/0956797610390386.

58 Staw, The Escalation of Commitment to a Course of Action, The Academy of Management Review, Vol. 6, No. 4, 1981, p.577–587. doi:https://doi.org/10.2307/257636.

59 Brockner, The Escalation of Commitment to a Failing Course of Action: Toward Theoretical Progress, Academy of Management Review, Vol. 17, No. 1,1992, pp.39–61. doi:https://doi.org/10.5465/amr.1992.4279568.

60 Salter, Monsanto shareholders approve Bayer’s $57 billion takeover, AP News, 2016, Available at: https://apnews.com/monsanto-shareholders-approve-bayers-57-billion-takeover-7cf8ca54f66f454ca98b745108b5b219.

61 Farm Aid, Farmers Overwhelmingly Oppose Bayer Monsanto Merger, Farm Aid, 2018, Available at: https://www.farmaid.org/issues/corporate-power/farmers-overwhelmingly-oppose-bayer-monsanto-merger/

62 See note 42

63 Mano, Brazil agency says Bayer-Monsanto tie-up can hurt competition, urges conditions, Reuters, 2017, Available at: https://www.reuters.com/article/business/brazil-agency-says-bayer-monsanto-tie-up-can-hurt-competition-urges-conditions-idUSKCN1C91BT/

64 Neate, Bayer’s $66bn takeover bid of Monsanto called a ‘marriage made in hell’, The Guardian, 2016, Available at: https://www.theguardian.com/business/2016/sep/14/bayer-takeover-monsanto-66-billion-deal

65 Klobuchar, Klobuchar, Merkley, Senators Urge DOJ Antitrust Division to Conduct Thorough and Impartial Analysis of Bayer AG Acquisition of Monsanto Company, U.S. Senator Amy Klobuchar, 2017, Available at: https://www.klobuchar.senate.gov/public/index.cfm/news-releases?ID=B46520CA-8D6B-47D3-AD15-AFC33B9D8486

66 Nicola/Jennen, Bayer’s Monsanto deal faces big backlash in Germany, Houston Chronicle, 2016, Available at: https://www.houstonchronicle.com/business/article/Bayer-s-Monsanto-deal-faces-big-backlash-in-7781560.php

67 Hakim, Monsanto’s Roundup Faces European Politics and U.S. Lawsuits, The New York Times, 2017, Available at: https://www.nytimes.com/2017/10/04/business/monsanto-roundup-europe.html.

68 The Guardian, Roundup weedkiller ‘probably’ causes cancer, says WHO study, The Guardian, 2015, Available at: https://www.theguardian.com/environment/2015/mar/21/roundup-cancer-who-glyphosate-

69 Neslen, Monsanto banned from European parliament, The Guardian, 2017, Available at: https://www.theguardian.com/environment/2017/sep/28/monsanto-banned-from-european-parliament.

70 Pierson, Plaintiffs in U.S. lawsuit say Monsanto ghostwrote Roundup studies, Reuters, 2017, Available at: https://www.reuters.com/article/business/plaintiffs-in-us-lawsuit-say-monsanto-ghostwrote-roundup-studies-idUSKBN16M066/

71 Quinn/Jones, An Agent Morality View of Business Policy, The Academy of Management Review, Vol. 20, No. 1, 1995, p.22. doi:https://doi.org/10.2307/258885.

72 See note 9

73 See note 51

74 See note 9

75 See note 8

76 Burger/Bellon, Bayer to pay up to $10.9 billion to settle bulk of Roundup weedkiller cancer lawsuits, Reuters, 2020, Available at: https://www.reuters.com/article/business/bayer-to-pay-up-to-109-billion-to-settle-bulk-of-roundup-weedkiller-cancer-law-idUSKBN23V2NO/.

77 BBC News, Bayer to pay $10.9bn to settle weedkiller cancer claims, BBC News, 2020, Available at: https://www.bbc.co.uk/news/business-53174513.

78 France 24, Weedkiller Roundup banned in France after court ruling, France 24, 2019, Available at: https://www.france24.com/en/20190116-weedkiller-roundup-banned-france-after-court-ruling.

79 Reuters, German cabinet approves restricted use of herbicide glyphosate, Reuters, 2024, Available at: https://www.reuters.com/world/europe/german-cabinet-approves-restricted-use-herbicide-glyphosate-2024-04-24/.

80 Finger/Möhring/Kudsk, Glyphosate ban will have economic impacts on European agriculture but effects are heterogenous and uncertain, Communications Earth & Environment, Vol. 4, 2023 doi:https://doi.org/10.1038/s43247-023-00951-x

81 Bennett, Government ministers should ban Roundup – not sing its praises, The Guardian, 2018, Available at: https://www.theguardian.com/commentisfree/2018/aug/14/roundup-government-uk-minister-ban-glyphosate.

82 Chazan, Bayer execs face investor heat after rare no-confidence vote, Financial Times, 2019, Available at: https://www.ft.com/content/0a6cc01c-69a3-11e9-80c7-60ee53e6681d.

83 Mariappan, Mergers and Acquisitions: The Human Issues and Strategies, Indian Journal of Industrial Relations, Vol. 39, No. 1, 2003, p.84–94.

84 Suraihi/Samikon/Suraihi/Ibrahim, Employee turnover: Causes, Importance and Retention Strategies, European Journal of Business and Management Research, Vol. 6, No. 3, 2021, p.1–10, doi:https://doi.org/10.24018/ejbmr.2021.6.3.893.

85 Loth, Is There a Dark Side to Divestitures? Employee Commitment after Corporate Divestitures. Academy of Management Proceedings, 2022(1), 2022, doi:https://doi.org/10.5465/ambpp.2022.16771abstract.

86 Hennig/Loth/Wolff, No Light without Shadow? Implications of Divestitures from the Employee Perspective. Academy of Management Proceedings, 2023(1), 2023, doi:https://doi.org/10.5465/amproc.2023.18387abstract.

87 See note 76

88 Linhartová/Urbancová, Employee turnover and maintaining knowledge continuity in large and small organisations, Ekonomická revue - Central European Review of Economic Issues, Vol. 14, No. 4, 2011, p.265–274. doi:https://doi.org/10.7327/cerei.2011.12.03.

89 Trautwein, Merger motives and merger prescriptions, Strategic Management Journal, Vol. 11, No. 4, 1990, p.283–295.

90 Jemison/Sitkin, Corporate Acquisitions: A Process Perspective, The Academy of Management Review, Vol. 11, No. 1, p.145, 1986, doi:https://doi.org/10.2307/258337.

91 Abdulai/Ibrahim, Merging Cultures in International Mergers and Acquisitions: A Case Study of Lenovo’s Acquisition of IBM PC Division. Journal of Intercultural Communication, Vol. 16, No. 2, 2016.

92 Mujajati/Ferreira/Plessis, Fostering organisational commitment: a resilience framework for private-sector organisations in South Africa, Frontiers in Psychology, Vol. 15, 2024. doi:https://doi.org/10.3389/fpsyg.2024.1303866.

93 See note 82

94 Smeulders/Dekker/Abbeele, Post-acquisition integration: Managing cultural differences and employee resistance using integration controls, Accounting, Organizations and Society, Vol. 107, 2023, doi:https://doi.org/10.1016/j.aos.2022.101427.

95 Datta, Organizational fit and acquisition performance: Effects of post-acquisition integration, Strategic Management Journal, Vol. 12, No. 4, 1991, p.281–297, doi:https://doi.org/10.1002/smj.4250120404.

96 Teerikangas/Véry, Culture in Mergers and Acquisitions: A Critical Synthesis and Steps Forward, The Handbook of Mergers and Acquisitions, Oxford University Press, p.392–430, 2012.