Market Update on Transactional Risk Insurance in Continental Europe

1. Introduction

The European Transaction Risk Insurance (TRI) Market has seen many surprises over the last years in a turbulent M&A market environment. Below we will briefly explain what happened in the warranty & indemnity (W&I) insurance segment and the contingent risk insurance (CRI) seg-ment of the European TRI market in 2020 and the first half-year of 2021. Moreover, we will summarize the most import trends with respect to W&I insurance and CRI products and their usage in European M&A transactions.

2. Market Update

After years of increasing demand in both the W&I insur-ance segment as well as the CRI segment, the COVID-19 pandemic first appeared to bring such development to a halt when the European M&A market almost shut down in Q1 2020. Fears of a lost year and a dried out future M&A market quickly vanished when the market activity swiftly picked up again in the second half of 2020 leading to unexpectedly positive results despite the global pan-demic being in full rush. Fortunately, the M&A market remained busy throughout all 3 quarters of 2021, which had a positive effect on the TRI market being highly dependent on the M&A market activity.

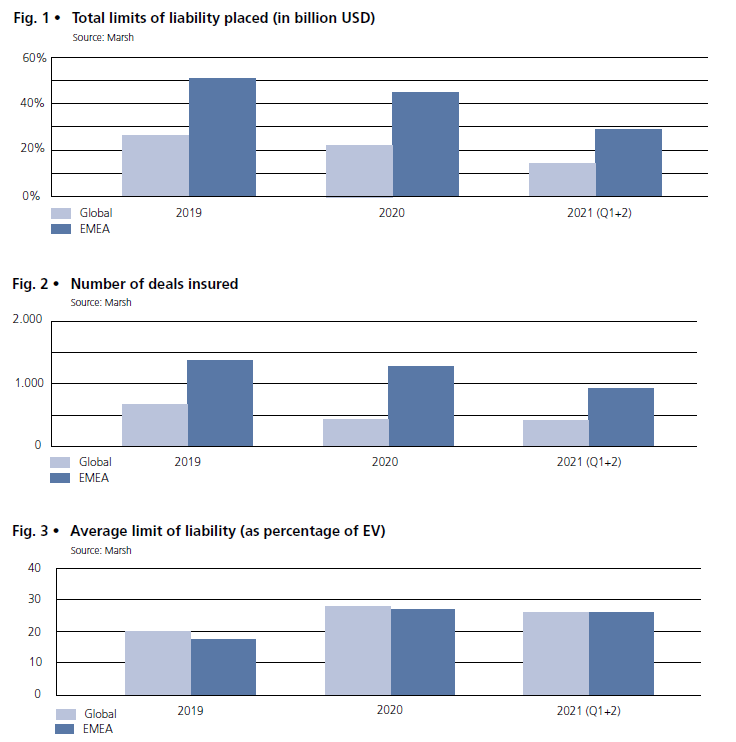

The total TRI limits (W&I insurance and CRI taken together) placed by Marsh on a global level as well as on EMEA level reflect such positive market development.

Given that the Fig.1 reflects for 2021 only the first half-year, it is highly likely that the total limits placed in the full year will exceed the 2019 level.

The positive market development also had an effect on the number of deals insured through TRI products both on a global level as well as the EMEA level.

Again, Fig.2 only reflects for 2021 the first half-year. In this period, we saw more EMEA deals insured through TRI products as in the full year 2020 (even though the total limit placed in 2021 is still less than 2020). We expect that the total number of deals in-sured in 2021 will even exceed the high 2019 numbers.

The EMEA insurance market also benefited from higher limits of liability purchased for W&I insurance compared to prior years. As shown in the Fig. 3, in average buyers chose significantly higher W&I insurance limits in 2020 as compared to 2019. The average limit of liability chosen by insurance buyers remained on a high level also in the first half-year of 2021. On a global level, we could see a similar trend.

In terms of costs, the European W&I insurance segment did not see any significant changes in 2020 and 2021 (first half-year) and premia remained stable in this period with the exception of the UK market where we saw a moderate increase of premia. In contrast, premia for CRI products slightly decreased d the same period mainly due to widening competition among insurers offering CRI products.

3. Product Trends

In the W&I insurance segment, the trend towards broader coverage as seen in the last years continued also in 2020 and 2021 (first half-year) due to a fierce competition amount W&I insurers. As a result, several coverage exclusions of W&I policies became narrower or fell away entirely (e.g. data protection aspects) in many transactions. Furthermore, a general exclusion for losses relating from COVID-19 effects that had been introduced by certain insurers when the crisis hit Europe in 2020 has been replaced by the insurers’ requirement that the buyer reviews COVID-19 effects on the target as part of the due diligence exercise. This requirement comes as no surprise as it merely reflects general prin-ciples of W&I insurance. We also saw a positive effect on coverage due to the fact that insurers became increas-ingly open and use to so-called blind spot coverage to offer coverage for areas (e.g. certain tax types or jurisdic-tions) that have not been (properly) reviewed in the buy-side due diligence exercise. To offer blind spot coverage the insurers usually required additional premium.

Another continuing trend in the European W&I insurance segment is the increased usage of synthetic coverage elements in W&I policies. Buyers purchase such coverage enhancements to bridge the gaps left by seller-friendly warranty concepts applied in many acquisition agree-ments. The most important synthetic coverage elements in W&I policies are broader loss definitions, the elimination of knowledge qualifiers in warranties through so-called knowledge scraping and synthetic tax coverage used in transactions where the seller does not offer a tax indem-nity. Full synthetic W&I policies remain the exception to the rule mainly because the European distressed M&A market has not yet become as busy as expected.

With respect to the CRI segment, we currently see in Europe a growing use of CRI products beyond M&A situations to cover risks that stem from the insured’s day-to-day operations, such as tax risks or potential litigations. With respect to tax insurance in particular, we notice that the number of insurers offering such insurance has greatly expanded in the past years. In the European marketplace alone, we now see excess of 15 insurers interested in tax risks. Moreover, the insurers’ in-house tax expertise has grown over the last years. As a result, the insurers nowadays have a better understanding of more difficult tax risks even insuring in certain instances tax issues that are under active investigation by tax au-thorities.