1. Executive Summary

If activism campaigns seemed to have slowed down for a while during the Covid epidemic, attacks are on the rise again, laying the groundwork for new trends for this year 2021. The structure of the campaigns, their purpose, but above all the profile of the attackers, are changing. Today, shareholders of all types – institutional investors, hedge funds and full-time activists – require more from Boards of Directors, asking for direct engagement and explanation for lack of performance. More than ever, Directors need to understand their shareholders.

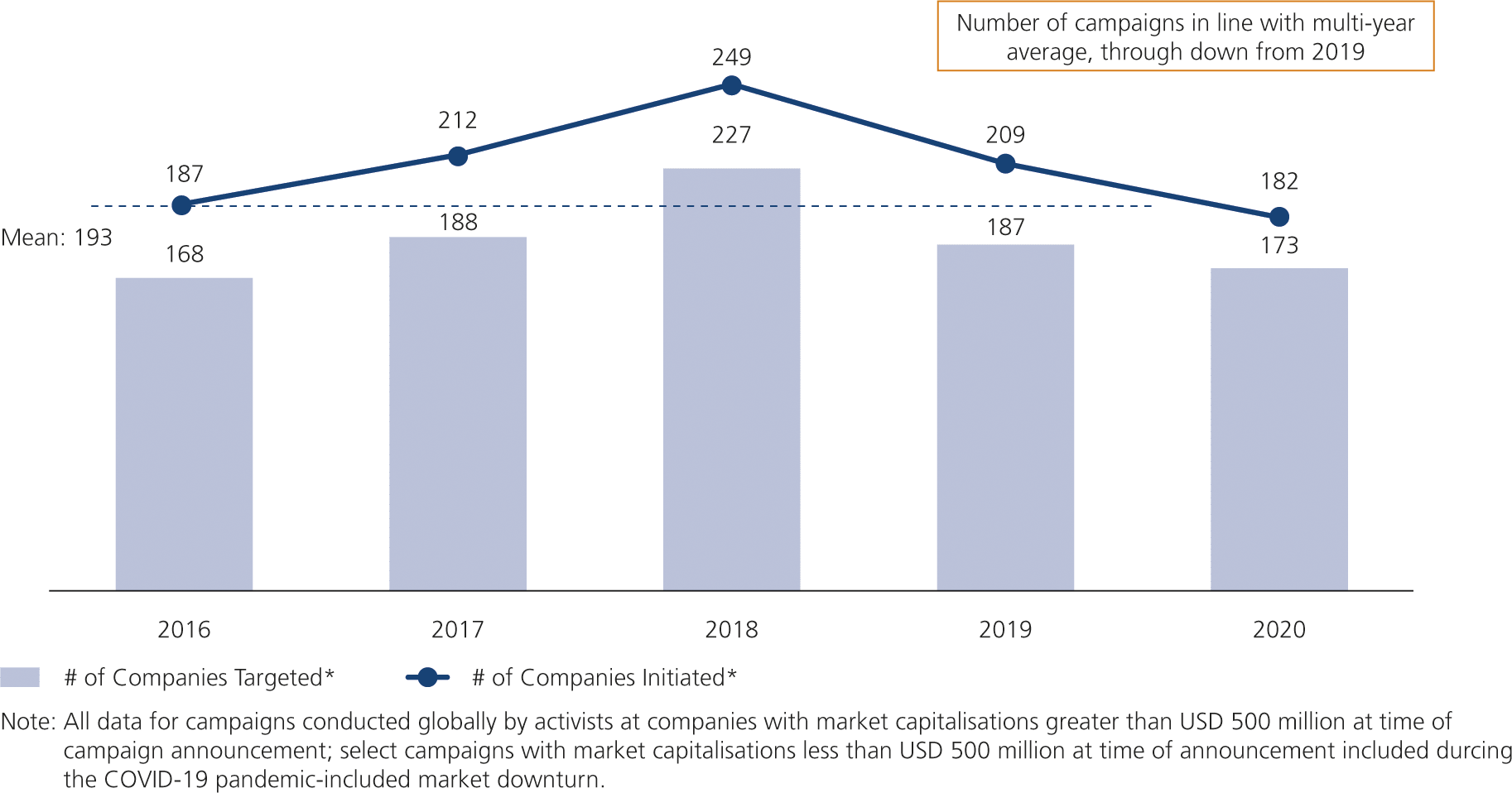

2. 2020, a Year of Contrasting Dynamics

At first glance, from a global perspective, 2020 appears to be the least active year in the last five years: 182 campaigns worldwide (a 13% drop from the previous year) for USD 40 billion deployed, against USD 42.3 billion in 2019, far from the record number of USD 67.2 billion in 2018. But since the end of summer, the campaigns have roared back indeed. One figure speaks for itself: in the fourth quarter of 2020, 57 new campaigns were launched worldwide, an increase of 128% compared to the previous quarter. Let’s look back at this special year.

In March 2020, activism came to an abrupt halt, in line with an unprecedented international context. The shock wave spared no part of the economic activity, and Covid brought activist campaigns to a near halt. This occurred in a year that started off with a bang in January and February, with 13.1 billion mobilized through 42 activist campaigns. In the wake of a disrupted M&A market, the environment of total uncertainty and high volatility did not provide a favorable environment for activist shareholders, who lost part of their room for maneuver. Yet, as early as May 2020, a rebound was underway – particularly in the United States. And if the figures for the first half of the year showed a downward trend with 100 campaigns, i.e. 10% less over the year, the “pause” seemed to be waning: the last months of the year confirmed the trend.

Source: Lazard‘s Annual Review of Shareholder Activism – 2020 based on FactSet, press reports and public filings

United Kingdom had the most campaigns in fiscal year 2020 with 21 of them, ahead of Germany and France with 10 and 7 offensives, respectively. The performance on the UK market, despite a slight decline compared to the previous year, could be explained by a strong acceleration of campaigns in the second half of 2020.

Who are the activists’ targets? In Europe, small and mid-caps (less than USD 2 billion to USD 5 billion in capitalization) represented more than 6 out of 10 campaigns (64%, i.e., 10 points higher than the average of the previous three years). As for most targeted sectors, we observe in Europe an over-representation of industrials (33% against 18% in the USA), while technology companies, which led American targets (19%), only account for 5% of European cases. In contrast, the consumer sector – hit hard by the economic collapse – is more under attack in Europe (in third place after the industrial and financial sectors) than in the US.

3. Shareholders Take the Lead

Year 2020 proved that activism has irrevocably moved from the fringes of shareholder register to the center. Alongside “pure players” such as hedge funds, “traditional” shareholders are more and more determined to shake up companies. Deference to management a thing of the past. Today, shareholders do not hesitate to exert pressure or seek to replace management and review strategy when necessary to stimulate value creation. For this group of investors, activism tactics are only tools to serve an end, not the centerpiece of their investment strategy.

Source: Lazard‘s Annual Review of Shareholder Activism – 2020 based on FactSet, press reports and public filings

The unprecedented increase in activist campaigns in Europe in 2020 was thus led by traditional asset managers, long-term holders who were not previously considered to be agitators. By way of comparison, in 2018 and 2019, full-time activists led the vast majority, i.e. 60%, of European campaigns, falling to only 35% by 2020. At the same time, traditional asset managers almost doubled their attacks, from 27% of the total in 2018-2019 to almost 50% of all campaigns last year.

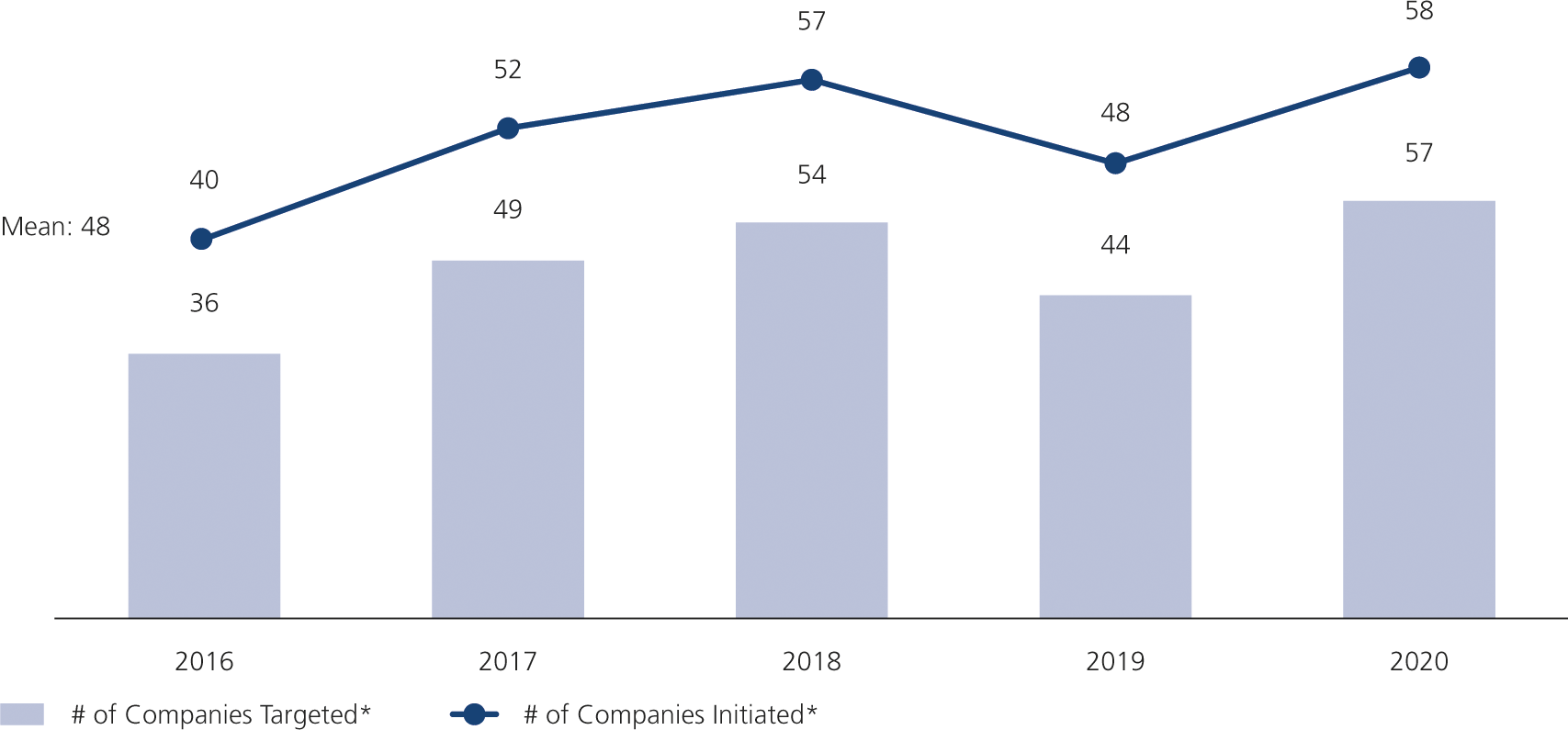

4. The New European Situation

Apathy in the spring was particularly severe in the United States, the historically dominant playground of shareholder activism. As a result of the mechanical contrast effect, it was the market where growth was the most significant at the end of 2020: 200% increase compared to the third quarter. With 53% market share in Q4, the American continent remained the most active; but, for all that, Europe completed a record year in this area with the highest level of campaigns ever. Figures speak for themselves: 58 new individual campaigns were launched, 21% more than in 2019. This continent-wide increase was largely because the year began and ended at a blistering pace, with no less than 22 campaigns in the fourth quarter alone. In the first quarter, Europe even accounted for 71% of the activity, against 59% in the same period of the previous year.

There is also a real change of mentality taking place throughout Europe. Shareholders consider that they are not only investors, but also active, committed and demanding owners. As such, they specifically focus on strategy. Campaigns to influence a company’s strategy increased more than 3.5 times in 2020. By the end of the year, they accounted for almost a quarter of all activist situations in Europe.

Equally striking is the increased pressure on senior management. Historically, in companies targeted by an activist, there was a 10% chance that the company’s leader would change within six months, which was twice the rate of normal executive turnover. By 2020, this turnover rate rose to over 20% in just six months (four times the normal rate).

As a result of this shareholder power increase, Boards of Directors will probably more often require company management to define and communicate a strategic plan in line with shareholders’ expectations. Otherwise, shareholders may want to fulfill this mission themselves, and will not hesitate to speak out publicly to achieve their goals.

5. ESG, a Growing Concern of Activist Campaigns

The past twelve months have also shown how ESG principle fulfilled its promise to become the next shareholder battleground.

ESG is impacting investor portfolio decisions, as more investors include ESG considerations in investment screening and portfolio risk management tools. Analysis of the Euro STOXX 600 suggests that the largest active managers allocate nearly 10% more capital to low ESG risk companies than to medium ESG risk ones. In addition, 2020 saw a more than 100% increase in the number of European companies targeted with ESG resolutions at their AGM, compared to 2018–19.

It is not surprising then, that activists adjust their strategies to adapt to ESG issues. Campaigns focused on ESG, in which stakeholders’ interests are emphasized alongside (or instead of) creating shareholder value, attract more attention. TCI’s “Say on Climate” campaign and Bluebell’s “One Share ESG Campaign” are examples of funds that have used these ESG strategies to strengthen their reputation with investors and broaden their investment mandate.

Shareholders now expect Boards of Directors to manage ESG issues as fundamental risks for the company, and as risks inextricably linked to long-term strategy. For example, we can cite Vanguard’s warning ahead of the vote against corporate directors “whose progress on Board diversity is lagging behind market standards and expectations”. Or, Christophe Hohn, founder of the British fund TCI based on the “Say on Pay” model, campaigning for “Say on Climate” resolutions to be put on AGM agenda. Activists’ ability to take hold of these issues could already provide fertile ground for accelerating this type of campaign in 2021.

In 2021, how should boards of directors and corporate directions respond to these growing and intensifying demands while considering new, post-Covid shareholder dynamics?

6. To Guard against Activism: Action-based Programs rather than Plans and more Attention to Best Practices

If the old advice “Don’t surprise your shareholders” is still valid, it would be appropriate in 2021 to add to it: “Don’t let your shareholders surprise you”.

Thus, action programs will be even more successful if they are based on a realistic view of investors’ feedback, also providing an additional mechanism to detect problems before they hit the headlines. Likewise, a dialogue between shareholders and independent directors, data-based analyses of the investor landscape and the shareholder base, evaluations of Shareholder Sentiment by the Board of Directors, an investor relations policy linking long-term strategy and ESG issues, Specialized Board Committees dealing with ESG strategy or issues, ESG rating optimization, ESG branding, and shareholder targeting... are just a few of the many best practices in governance and shareholder communication that each Board of Directors has at its disposal in 2021.

While, in a way, it has never been more difficult to be a director, this changing environment also creates opportunities. But on the positive side, management teams and Boards of Directors that have a detailed understanding of shareholders’ expectations, and that quickly adapt to the changing business landscape and the dynamics of ESG factors, will capture a greater share of investments. The higher the requirements, the greater the rewards.