M&A market 2020: Solid year despite Corona

1. Introduction

Global transaction volume in the fourth quarter of 2020 was USD 1,093 billion, up 17 per cent on the previous quarter and 21 per cent on the fourth quarter of the previous year. This development was mainly driven by a significant recovery in the Americas and Europe. Volume in the Americas increased by 36 per cent quarter-on-quarter, while Europe saw growth of around 21 per cent. In contrast, the transaction volume in Asia fell slightly by 2 per cent compared to the previous quarter.

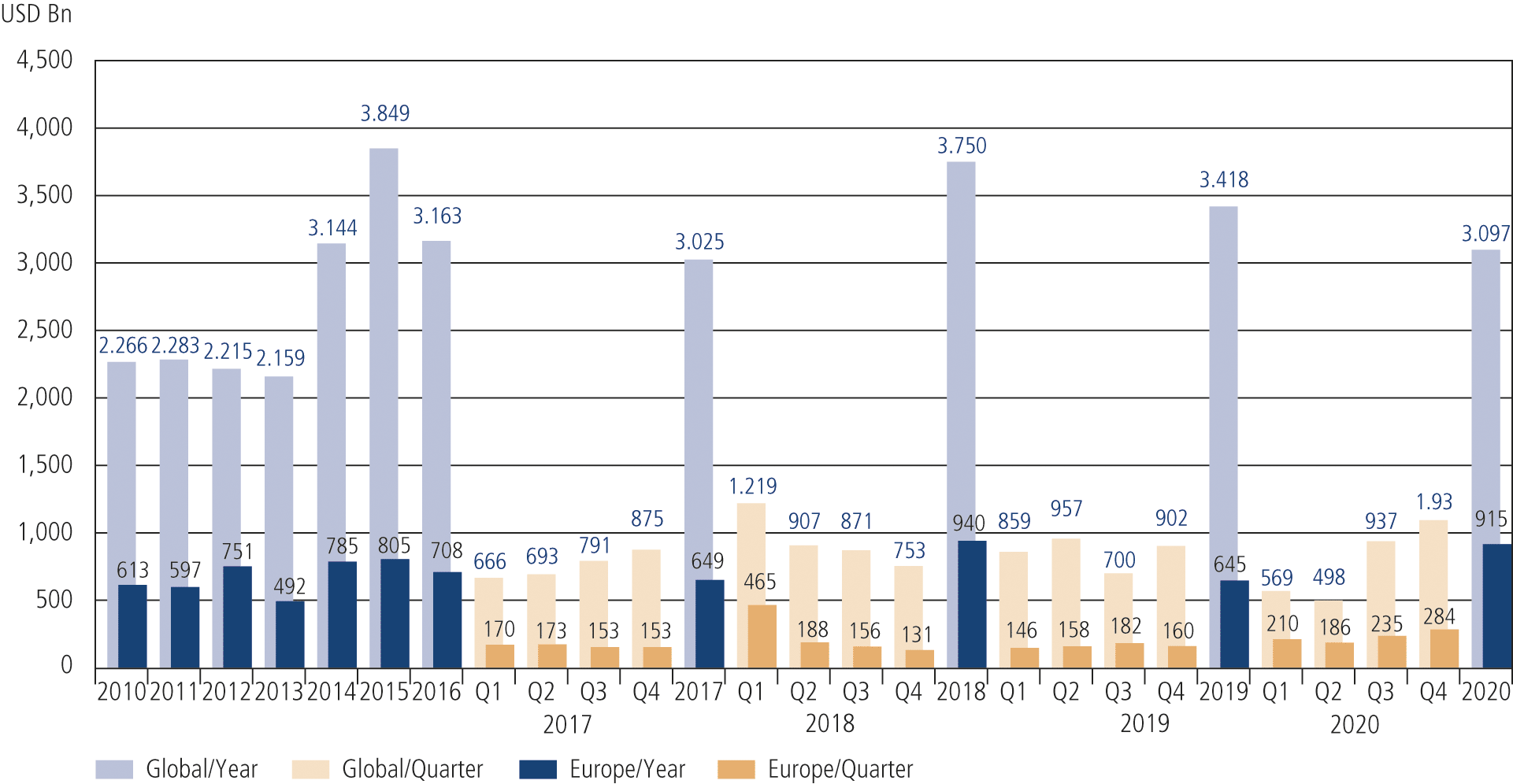

Compared to the previous year, the global transaction volume was USD 3,097 billion, which corresponds to a decline of 9 percent. The volumes in America and Asia were significantly below the average of the last five years, whereas Europe was significantly above.

2. Macro Environment

The Dow Jones again recorded solid growth in the fourth quarter of the year and reached the 30,000-point mark for the first time on 24 November 2020. The positive development continued thereafter and the Dow Jones closed the year at an all-time high of 30,606 points. Compared to the previous quarter, it gained around 10 per cent and was 7 per cent higher at the end of December than in the same quarter of the previous year. Volatility increased again compared to the previous quarter and clearly exceeded the previous year’s value. At 1,084 points, the standard deviation was above the value of the third quarter (831 points) and clearly above the value of the previous year (689 points).

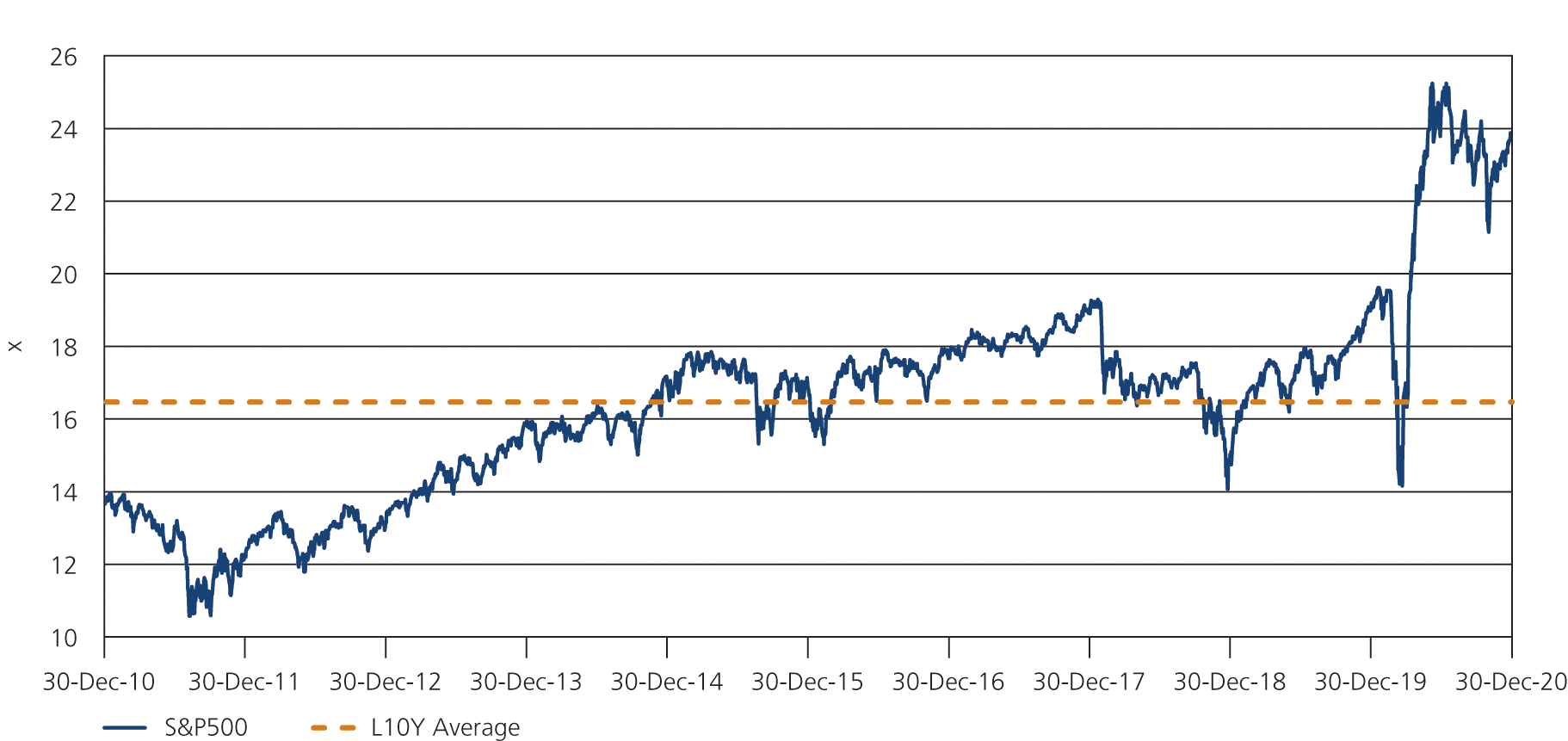

The S&P 500 ended the quarter with a price-to-earnings (P/E) ratio based on 12-month earnings expectations of 23.8x, which is below the peak of recent months but still significantly above the average of 16.5x over the past 10 years. This value is largely due to the drop in earnings expectations in the wake of the Corona crisis, which have fallen more sharply than prices. The renewed increase in the P/E ratio compared to the third quarter, when it was 23.0x, is due to the rise in company valuations following Joe Biden’s victory in the US elections on 03 November and the approval of the first Corona vaccines in December.

Source: Capital IQ

After the slump in global economic activity in the first half of 2020, GDP in the OECD countries rose by 9.0 percent in the third quarter compared to the second quarter of 2020. Compared to the same quarter of the previous year, GDP nevertheless fell by 4.1 percent. In its latest Economic Outlook, the OECD expects global economic output to grow by only 4.2 per cent in 2021, a slight downward revision from the 5 per cent growth forecast last quarter. This means that global GDP will still reach the pre-crisis level by the end of 2021. For 2022, the OECD expects slightly lower economic output growth of 3.7 per cent. However, the development of the coming quarters depends heavily on the further course of the Corona pandemic, in particular whether the prospects of a successful distribution of the vaccine will lead to a sustained improvement in consumer and business confidence. If there is a stronger improvement, economic growth could recover markedly, rising to 5 per cent in 2021 and 5.5 per cent in 2022. However, if the outlook were to deteriorate, the OECD projects economic activity to weaken by 2.75 per cent in 2021 and 1.5 per cent in 2022 compared to the central forecast. Although the approval of the first vaccines is a hopeful prospect, the OECD continues to urge governments to maintain support measures for the time being and to act decisively to provide a positive impetus to economic recovery.

After a sharp decline in GDP and a drastic increase in unemployment in the USA in the first half of the year, the economy recovered in the third quarter of 2020 and grew by 7.4 percent compared to the previous quarter, according to the OECD. For 2020 as a whole, GDP is expected to decline by 3.7 per cent. In its Economic Outlook, the OECD expects GDP in the US to grow by 3.2 per cent in 2021 and 3.5 per cent in 2022. The OECD expects the unemployment rate to gradually decline again, but to remain elevated compared to the pre-Corona period. This continues to reflect the lack of activity, especially in the sectors most affected by the pandemic, such as hospitality and transportation.

The Federal Reserve (FED) led by Jerome Powell announced at its December meeting that it will continue to keep the key interest rate at around 0 per cent, probably until at least the end of 2023, and will only consider a change in the interest rate if inflation remains at a level slightly above 2 per cent for an extended period of time. The FED also announced that it will continue to maintain its USD 120 billion per month bond-buying programme until “substantial further progress” is made towards full employment as well as price stability. As a result, USD 40 billion will flow into mortgage-backed securities each month and another USD 80 billion into US Treasury bonds. Contrary to the proposals of some economists to buy even more government bonds, for example to reduce interest rates on corporate bonds or mortgages, the Fed remains faithful to the current mix of purchases.

The fourth quarter in the USA was marked by the presidential election on 03 November 2020, in which Democrat Joe Biden prevailed over incumbent US President Donald Trump with 306 of the 538 votes. Biden became the first Democrat since 1992 and 1996 to win presidential elections in the traditionally Republican-dominated states of Georgia and Arizona, respectively. He was also the first candidate to win the election nationwide since 1960 excluding Ohio and since 1992 excluding Florida. The 59th presidential election also saw a historically high turnout. According to the United States Elections Project, voter turnout was 66.7 percent, the highest since the US presidential election in 1900. In total, around 160 million Americans exercised their right to vote. The high turnout was partly due to the large number of votes cast before 3 November 2020. One week before the election, more than 70 million voters cast their ballots by absentee or early voting, the highest figure since records began. The Democrats in particular were able to mobilise their voters to cast early ballots. Although Donald Trump had himself voted by absentee ballot in the US presidential primaries in March 2020, he criticised it since April 2020 and repeatedly claimed that absentee ballots would lead to voter fraud. Furthermore, there were repeated indications that Trump would not accept defeat in the election, which led to political uncertainty in the months leading up to the election. Consequently, it was no surprise that after the elections on 03 November there were a large number of lawsuits from Trump’s election office to prevent the counting of votes by legal means. However, these largely came to nothing. In the election for the United States Senate taking place at the same time, 33 of the 100 Senate seats were elected regularly, as well as a special election in Georgia and in Arizona. Initially, the Democrats gained only one seat, falling just short of a majority in the Senate with a total of 48 seats. However, since the Democrats won the two run-off elections in the state of Georgia on 5 January 2021, the newly elected government under Joe Biden now has a majority in both chambers of parliament and can push through reform projects without the support of Republican representatives.

In the week following Election Day, stock markets in the USA rose significantly. This positive development is primarily due to three main factors. First, Biden is expected to provide more reliability in foreign policy and negotiate trade disputes more rationally than Donald Trump. Biden also repeatedly made it clear that he represents a foreign policy in which, on the one hand, the American heartland is a key focus, but which, on the other hand, also relies on alliances and international cooperation. Consequently, Joe Biden has in the past emphasised the desire for multilateral agreements, which tends to be a positive backdrop for stock markets. Secondly, Joe Biden is expected to take a more structured approach and stricter measures to combat the Corona pandemic. Moreover, in the market, the likelihood of another aid package increased after Biden’s victory. For example, Biden repeatedly advocated a billion-dollar aid package during his election campaign if he won the election. Third, the Democrats fell short of a majority in the Senate. Therefore, the implementation of the announced tax increases and stricter regulations seemed unlikely at first, as the Republicans are clearly against such plans, which was positively received by the markets. In his election programme, Biden promised his voters tax reforms and regulatory changes focusing on higher corporate taxation as well as financial support for working families. As a result, raising the corporate tax rate from 21 to 28 per cent, a minimum tax of 15 per cent for companies that generate more than $100 million in retained earnings and closing tax loopholes were an integral part of Biden’s election platform. In addition, Biden announced that he would regulate the low-wage sector more strongly, for example by raising the minimum wage nationwide from 7.25 USD to 15 USD.

In the fourth quarter, the number of Corona infections in the USA increased steadily from around 50,000 new infections per day at the end of September to over 200,000 new infections per day at the end of December. As a result, around 8 million people in the US were infected with the Corona virus at the end of December, representing around 2.4 per cent of the population. On 11 December 2020, the U.S. Food and Drug Administration (FDA) confirmed the emergency approval of the Covid vaccine BNT 162b2 from the US company Pfizer and the Mainz-based biotech company BioNTech. Since then, more than 5.3 million people in the USA have already been vaccinated against Covid 19 (as of 06 January 2021) and a total of more than 17.2 million vaccine doses have already been delivered to federal authorities. At the end of December, Democrats and Republicans finally agreed on a new Corona aid package. The aid package has a volume of USD 900 billion and includes, among other things, one-time payments of USD 600 to a large part of the American population and an increase in unemployment benefits of USD 300 per week.

Compared to the United States, the OECD continues to expect a stronger economic contraction of 7.5 percent for the euro area in 2020, although the forecast has improved by 0.4 percentage points compared to September. The OECD attributes this primarily to the comparatively strict and relatively long lockdowns in Europe. The European Central Bank (ECB) under Christine Lagarde announced after the latest meeting in mid-December that it would extend the PEPP bond-buying programme until the end of March 2022 and expand it by a further EUR 500 billion. Consequently, the volume of bond purchases increases to EUR 1,850 billion. It was also announced that key interest rates will remain unchanged. Other fiscal policy measures announced in December include the launch of three additional tranches of TLTROs, the increase in the maximum volume for TLTROs per credit institution, and the introduction of four tranches of the longer-term pandemic emergency refinancing operations (PELTROs).

For 2020, the ECB now expects inflation in the Eurozone to be 0.2 percent instead of 0.3 percent as in September. The forecast for 2021, on the other hand, remained unchanged at 1.0 per cent, while the medium-term forecast for 2022 was revised downwards from 1.3 per cent to 1.1 per cent. For 2023, inflation is forecast at 1.4 per cent. The projected increase in inflation in 2021 largely reflects base effects in HICP energy inflation related to the sharp fall in oil prices at the start of the global Covid 19 outbreak, and can also be attributed to the phasing out of the VAT cut in Germany. With regard to economic growth in the euro area, the ECB has slightly adjusted its forecast. For 2020, it now expects a decline of 7.3 per cent, instead of 8.0 per cent as in September. At the same time, however, the ECB lowered its growth forecast for 2021 from 5.0 per cent to 3.9 per cent, while the forecast for 2022 was raised from 3.2 per cent to 4.2 per cent. For 2023, the ECB expects economic growth of 2.1 per cent. The OECD assumes a decline in economic output of 5.5 percent for Germany in 2020 (estimate September 2020: 5.4 percent decline). At the end of the fourth quarter of 2020, the ifo Business Climate Index rose again after two months of decline, climbing to 92.1 points in December 2020. In the manufacturing sector in particular, the index increased significantly, rising to its highest sector-specific value since January 2020. The main driver of this positive development was optimism in the chemical industry as well as in mechanical engineering. In the services sector, the index recovered only slightly. While transport and logistics companies are exhibit more optimism, managers in the travel, hospitality and culture sectors in particular remain pessimistic. The business climate indicator rose significantly in the trade sector, mainly due to positive expectations of industry-related wholesalers. Compared to the previous months, the business climate in the construction industry remained unchanged.

In the fourth quarter of the year, British representatives and EU diplomats continued to negotiate a withdrawal and trade agreement in numerous meetings. In the meantime, it looked as if a hard Brexit was inevitable, as the end of the transition period on 31 December 2020 was steadily approaching without any great progress being made. On Christmas Eve, the UK and the European Commission finally agreed on a deal that is to come into force on 1 January 2021. However, the agreement is only provisional, as both the European Parliament and all 27 EU member states still have to approve the agreement after a thorough review. In addition, there are still many details that need to be worked out in working groups over the coming months. The British House of Commons approved the negotiated Brexit agreement only 6 days after the agreement on Christmas Eve with a large majority of 521 to 73 votes. This was no surprise, as both the Tory Party and the opposition Labour MPs had already announced that they would vote in favour of the agreement. The aim of the trade agreement is, among other things, to prevent tariffs and to reduce friction in the important economic relationship between the European Union and Great Britain to a minimum. Although, according to the trade agreement, there will be no tariffs on British goods in the future, British exporters will have to prove that the products are predominantly manufactured in Great Britain, which will burden the export with more formalities. In addition to provisions to ensure fair competition between Britain and the EU (e.g. uniform requirements on workers’ rights, as well as social and environmental regulations), EU fishing in British waters has recently been a major point of contention in the negotiations. Although fishing plays only a minor role economically, the two parties were unable to reach an agreement until shortly before the end of the negotiations. This was partly due to the negotiating focus of the British representatives, who emphasised control and sovereignty. Nevertheless, both the EU and the UK made concessions, resulting in EU fishermen having to give up only 25 per cent of historic fishing quotas in stages over a period of five and a half years. Originally, the EU had called for a longer transition period, while the UK wanted to reduce fishing quotas by 80 percent. After the end of the transitional phase, catch quotas are to be set in annual negotiations.

After the sharpest decline and subsequent sharpest increase in history in the first and second quarters of 2020, respectively, economic growth in China stabilised in the third quarter. In the fourth quarter China recorded a growth in economic output of 6.5 percent, which results in a growth rate of 2.3 per cent for the full year, making China the only major industrialised nation to record economic growth in 2020, although significantly lower than in previous years. However, the OECD forecasts that the Chinese economy will return to its old growth trajectory, growing at 8 per cent in 2021 and 4.9 per cent in 2022. New Covid 19 cases have reappeared in isolated cases, but the pandemic seems to be largely under control in most parts of the country. Investments, especially in infrastructure projects as well as real estate, have boosted growth in 2020. Exports have picked up noticeably due to demand for masks and other Covid 19-related materials, as well as goods in the information and telecommunications sectors. However, consumption has yet to recover from the slump caused by the virus. Although sales of luxury goods, for example, have picked up significantly, the lack of recovery in employment figures and falling household incomes suggest that a full recovery in consumption will be a long time coming.

3. The M&A Market in Q4 2020: Trends and Developments

In the fourth quarter of 2020, the global M&A transaction volume of USD 1,093 billion was around 21 percent higher than in the same quarter of the previous year. Compared to the third quarter, the volume increased by 17 per cent. The number of transactions in the fourth quarter increased by 22 per cent compared to the last quarter, resulting in a 5 per cent decrease in average volume. The number of transactions as well as the average volume are above the average of the last 5 years by 22 per cent and 4 per cent, respectively. Compared to the same quarter last year, the average volume increased by 8 per cent and the number of transactions by 12 per cent.

Source: Thomson Financial

For the year as a whole, the global M&A transaction volume of USD 3,097 billion represents a decline of 9 percent compared to the previous year. This means that despite interim fears of a weak M&A year, mainly due to the global Corona pandemic, a strong result was achieved in the end. This was due in particular to a high number of transactions in the third and fourth quarters. The number of transactions in the second half of the year reached a record high of 2,271, outperforming 2019 and 2018 by 7 per cent and 4 per cent respectively. The full-year decline in transaction volume of 9 per cent is due to the low number of transactions and a low average volume in the first half of the year caused by the uncertainty resulting from the Corona pandemic.

Looking at the individual regions, the transaction volume in Europe increased by USD 124 billion compared to the fourth quarter of the previous year. This corresponds to a growth of 78 percent. This increase is attributable to both a 65 percent rise in average volume and an 8 percent increase in the number of transactions compared to the same quarter of the previous year. Compared to the third quarter of 2020, the volume increased by around 48 billion USD or 21 percent.

Source: Thomson Financial

The US M&A market grew in the fourth quarter, both year-on-year and quarter-on-quarter. Transaction volume increased by $196 billion compared to the fourth quarter of 2019, a 49 per cent increase. This increase can be attributed to an 18 per cent increase in average volume and a 26 per cent increase in the number of transactions. Compared to the third quarter of 2020, volume increased by around USD 159 billion, or 36 per cent.

Source: Thomson Financial

In the Asian market, transaction volume fell by USD 78 billion, or around 29 per cent, compared to the fourth quarter of 2019. In this context, the average volume fell by 35 per cent, from USD 690 million to USD 446 million, while the transaction number increased by 9 per cent from 385 to 420 transactions. Compared to the previous quarter, a slight decline in transaction volume of 2 per cent to USD 187 billion was observed.

Source: Thomson Financial

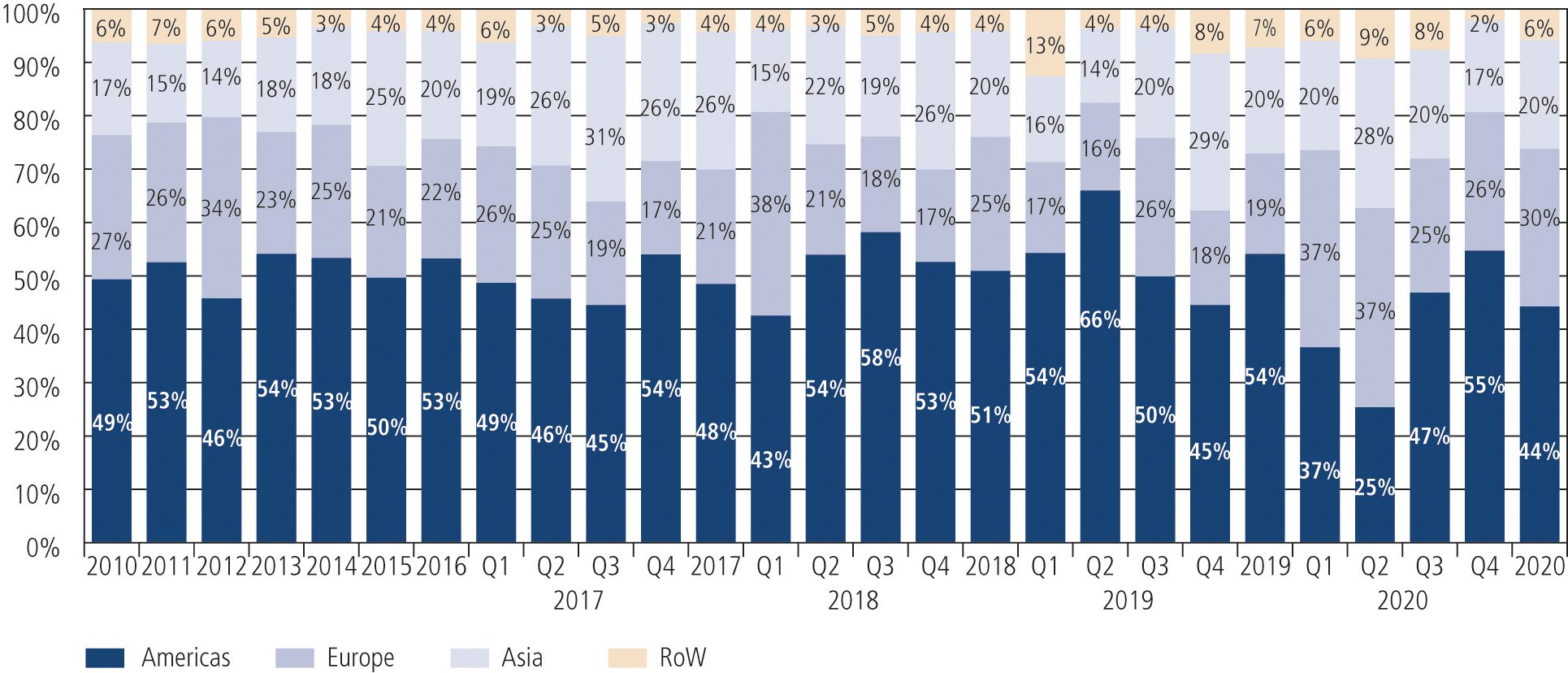

Expressed in market shares, 55 per cent for the American market, 26 per cent for the European market and 17 per cent for the Asian market emerged in the period under review at quarterly level.

Due to an ongoing recovery of the M&A market in America, the volume difference between Europe and America thus amounted to USD 314 billion in the fourth quarter. This volume difference is mainly due to a higher number of transactions in America. This means that America is once again the largest M&A market in the world in the fourth quarter. A look at the ten largest transactions in the past quarter makes it clear that US companies continue to make up the bulk. Among the target companies in the past quarter, there is only one European and one Asian company each compared to eight US companies.

Looking at 2020 as a whole, the transaction volume in Europe increased by USD 270 billion compared to the previous year, despite the Corona pandemic, which corresponds to an increase of 42 percent. This is primarily due to a significant increase in average volume of around 72 percent with a decrease in the number of transactions by 18 percent.

In contrast, the transaction volume in the Americas developed negatively year-on-year. Transaction volume fell by 26 per cent year-on-year to USD 1,371 billion, driven by a 2 per cent lower number of transactions and a 25 per cent lower average volume.

In Asia, a similar development as in the Americas emerged compared to the previous year. The transaction volume decreased by 7 per cent or USD 48 billion, which was caused by a 1 per cent lower number of transactions and a 6 per cent lower average volume.

Expressed in market shares, the annual figures are 44 per cent for the American market, 30 per cent for the European market and 20 per cent for the Asian market.

Source: Thomson Financial

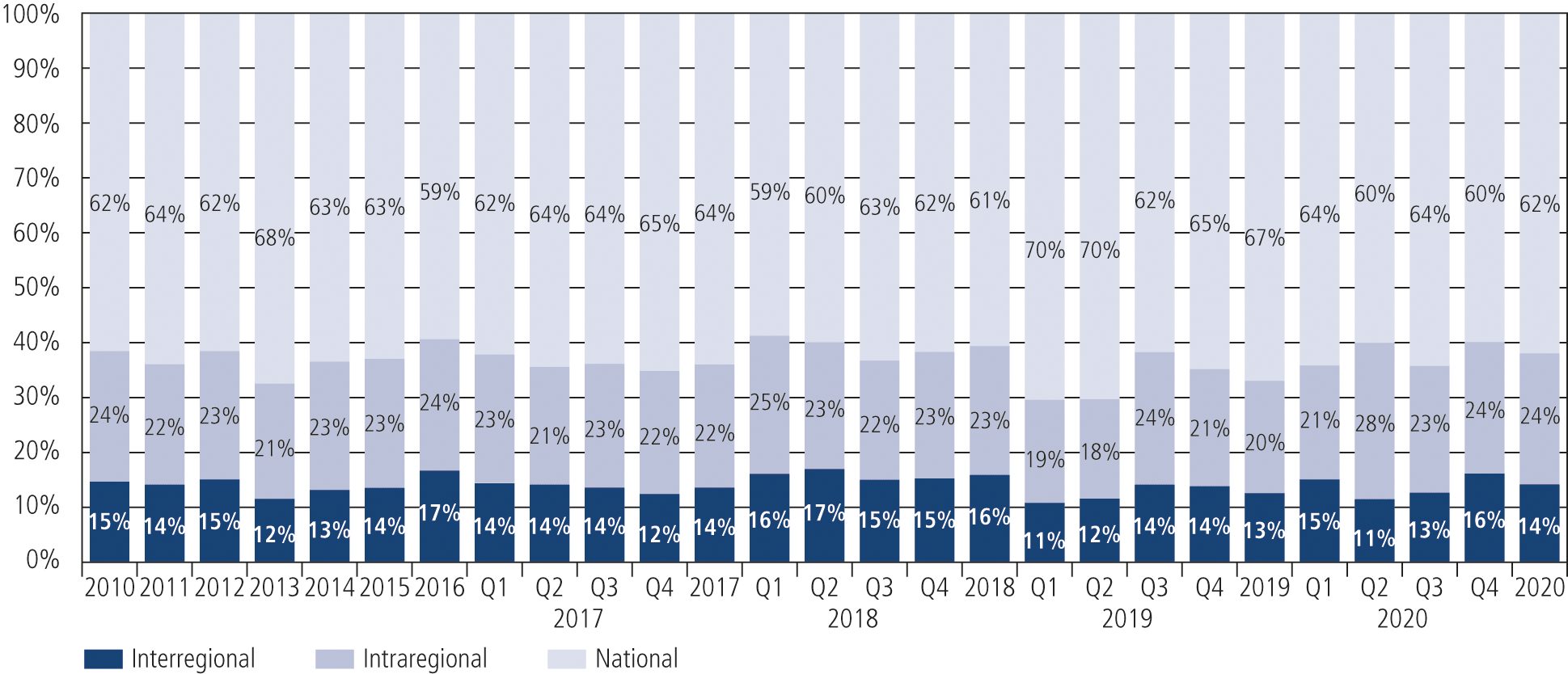

In the fourth quarter of 2020, there was a slight shift towards interregional transactions. The share of interregional transactions, i.e. transactions across continents, increased from 13 to 16 percent in the fourth quarter of 2020. The share of intraregional transactions also increased slightly by 1 percentage point to 24 percent, to the detriment of national transactions, whose share consequently fell from 64 to 60 percent. Accordingly, 40 percent of all transactions in the fourth quarter were cross-border activities, which is just above the average of the last decade of 37 percent. In the fourth quarter of the previous year, this share was 35 percent, while the share of national transactions was 65 percent. Looking at 2020 as a whole, the share of cross-border transactions is 38 percent, which is about 1 percentage point above the average of the previous 10 years.

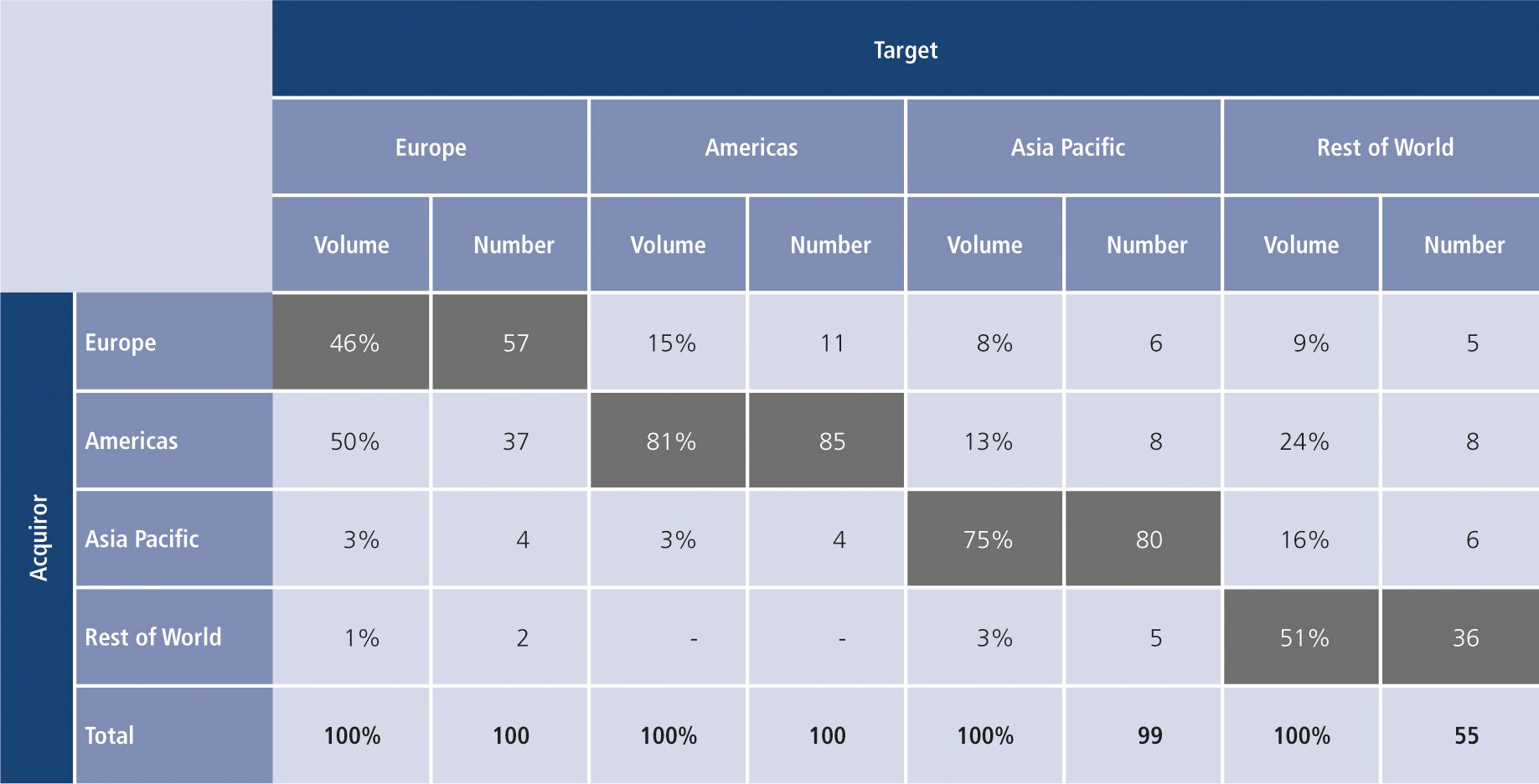

The figure below gives an overview of the 100 largest transactions per region and their distribution among the individual buyer regions. It shows that in Europe and the Americas, the target company and the buyer are from the same region in terms of volume in 46 and 81 per cent of the transactions, respectively. Compared to the third quarter of 2020, in which these values were 69 and 84 percent respectively, there was a strong shift back to interregional transactions in Europe and a slight shift in the Americas. European buyers were slightly more active in the Asian region in the fourth quarter of 2020, accounting for 8 per cent of the transaction volume compared to 1 per cent in the third quarter of 2020. Cross-border transaction volume with a European buyer and US target increased from 9 per cent to 15 per cent in the fourth quarter. American buyers’ share of total European volume increased from 30 per cent in the third quarter to 50 per cent in the fourth quarter. The percentage share of total transaction volume in Europe with an Asian buyer increased slightly from 1 to 3 per cent.

Source: Thomson Financial

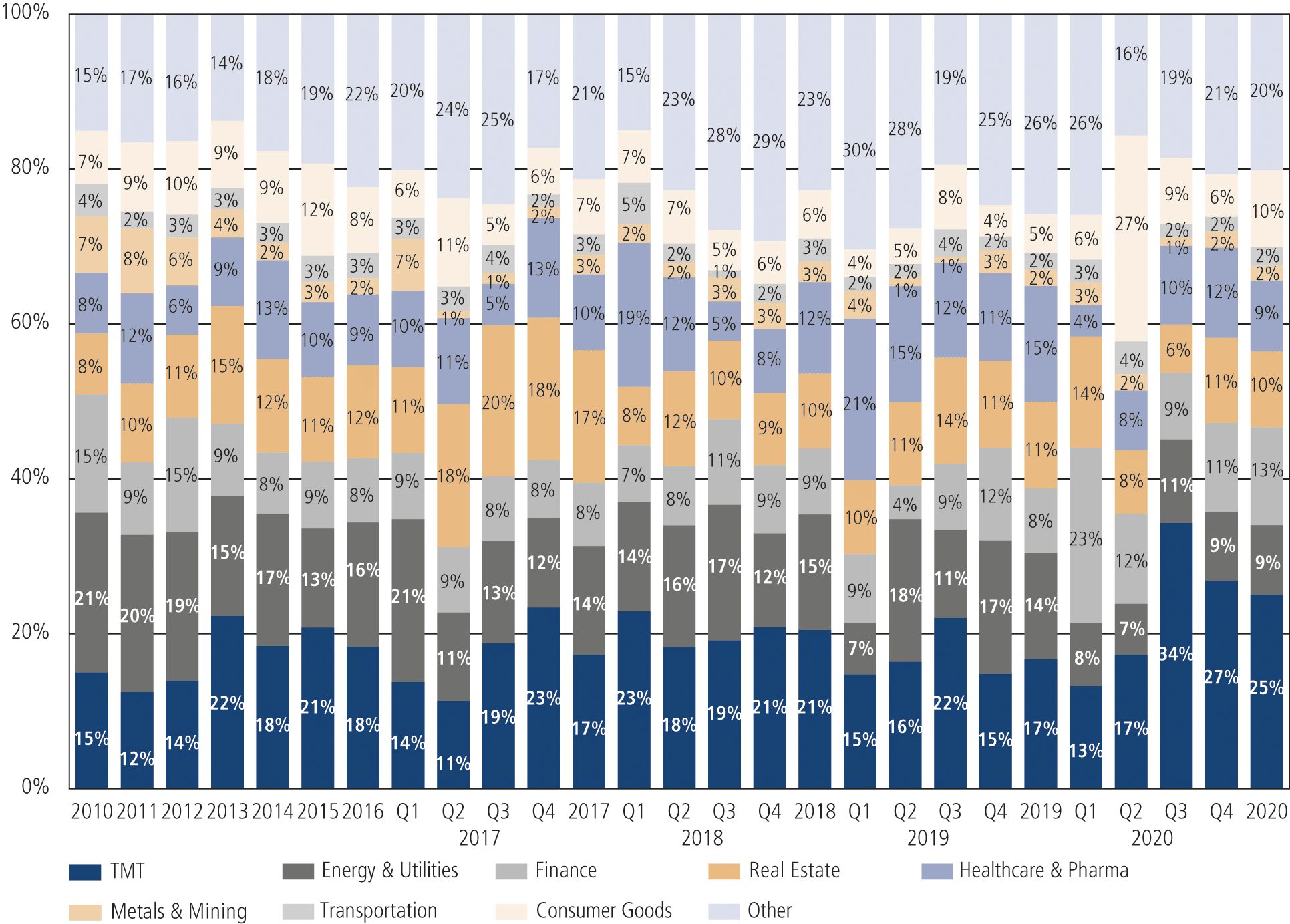

When looking at the M&A volume by sector, it is noticeable that compared to the third quarter of 2020, there was a decline in the TMT market share from 34 to 27 percent. Furthermore, a decline from 11 to 9 percent was observed in the Energy & Utilities sector. In contrast, there was a noticeable increase in the percentage shares of the Finance, Real Estate and Healthcare & Pharma sectors. In the Other sector, an increase from 19 to 21 percent was also observed compared to the previous quarter. The Consumer Goods sector shows a slight decline of 3 percentage points in the fourth quarter of 2020. The market shares of the Transportation and Metals & Mining sectors remained virtually unchanged in the quarterly view.

Source: Thomson Financial

Looking at 2020 as a whole, the TMT, Consumer Goods & Finance sectors in particular were able to increase their market share. While the market shares of the Transportation, Metals & Mining and Real Estate sectors remained virtually unchanged, the Energy & Utilities, Healthcare & Pharma and Other sectors recorded a decline.

In the fourth quarter of 2020, the largest announced transaction was the acquisition of IHS Markit Ltd. (IHS) by S&P Global Inc. (S&P) with a transaction value of USD 43.5 billion. The combination of the complementary product portfolios will allow S&P to offer its clients a broader range of services for a variety of industries directly from a single source following the acquisition. In addition, the merged company will have a presence in several areas with high growth potential and will be able to draw on its combined innovation and technology expertise. The transaction, in which IHS shareholders will receive 0.2838 S&P shares per share, will be fully equity financed. As a result, IHS shareholders will own 32.25 per cent of the combined company, whereas S&P shareholders will hold 67.75 per cent. The data industry has been marked by consolidations for some time, with the London Stock Exchange Group last year announcing the acquisition of Refinitiv, a joint venture between Blackstone and Thomas Reuters, for $27 billion.

Overall, the ten largest deals this quarter accounted for about 20 per cent of the total volume with an aggregate volume of USD 224 billion, a decrease of 8 percentage points compared to the previous quarter. The number of megadeals with a volume of more than USD 10 billion remained unchanged at 10. The number of national transactions among the ten largest deals rose from six to eight. As in the last quarter, the TMT sector was particularly well represented with three of the 10 largest transactions. The following transactions are particularly noteworthy:

• AstraZeneca announced in December that it would acquire 100 per cent of the shares of Alexion Pharmaceuticals. With a transaction volume of USD 39.6 billion, this would be the largest acquisition since AstraZeneca was founded in 1999. Alexion is a biotech company based in Boston, USA, and specialises in drugs for the treatment of rare diseases, such as Paroxysmal Nocturnal Hemoglobinuria (PNH). Through the acquisition, AstraZeneca aims to strengthen the field of immunology and the treatment of rare diseases in particular.

• On 1 December, Salesforce.com announced the USD 27.5 billion acquisition of Slack Technologies, a leading provider of digital communication solutions. Salesforce plans to integrate Slack into its existing portfolio of software solutions in order to strengthen its competitiveness, for example against CRM rival Microsoft, which was able to gain more than 70 million new users with Teams in the wake of the Corona pandemic. The transaction will be financed with a combination of cash (USD 26.70 per Slack share) and newly issued shares worth USD 10.9 billion.

• ConocoPhillips’ USD 12.9 billion acquisition of Concho Resources, a producer of shale oil and shale gas, was another transaction in the Energy & Utilities sector among the top 10 in the fourth quarter of 2020. As a result of the transaction, ConocoPhillips more than triples its acreage in the Permian Basin, the world’s most lucrative shale oil field. With the acquisition of Concho, which will be financed exclusively with shares, ConocoPhillips also wants to save operating and development costs.

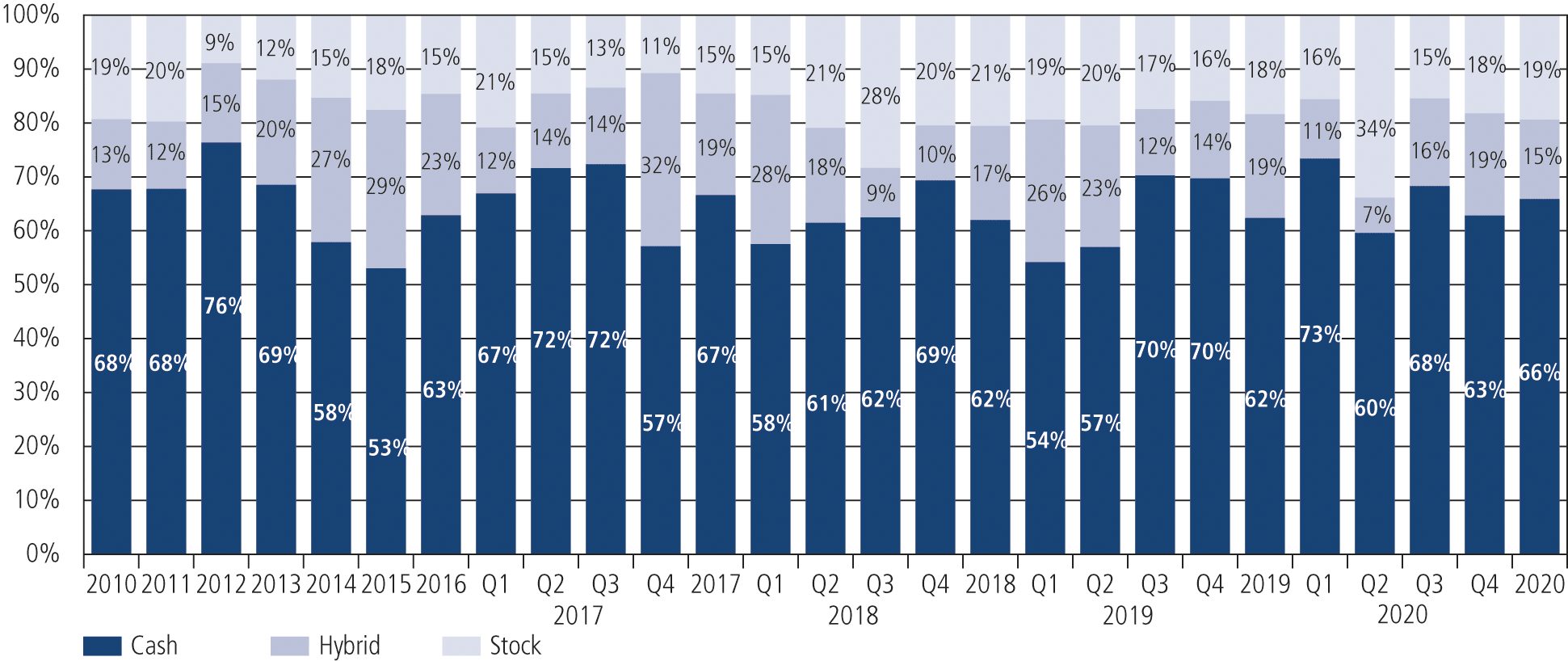

63 percent of the total transaction volume in the fourth quarter of 2020 was financed by cash, thus a decrease of 5 percentage points compared to the previous quarter can be observed. In contrast, the share of equities as a means of financing increased from 15 to 18 percent compared to the third quarter of the year. The share of transactions financed by a mix of cash and shares also increased by 3 percentage points to 19 percent. Looking at the annual statistics, the share of transactions financed with cash increased from 62 percent to 66 percent, whereas the share of transactions financed with hybrid capital decreased from 19 percent to 15 percent.

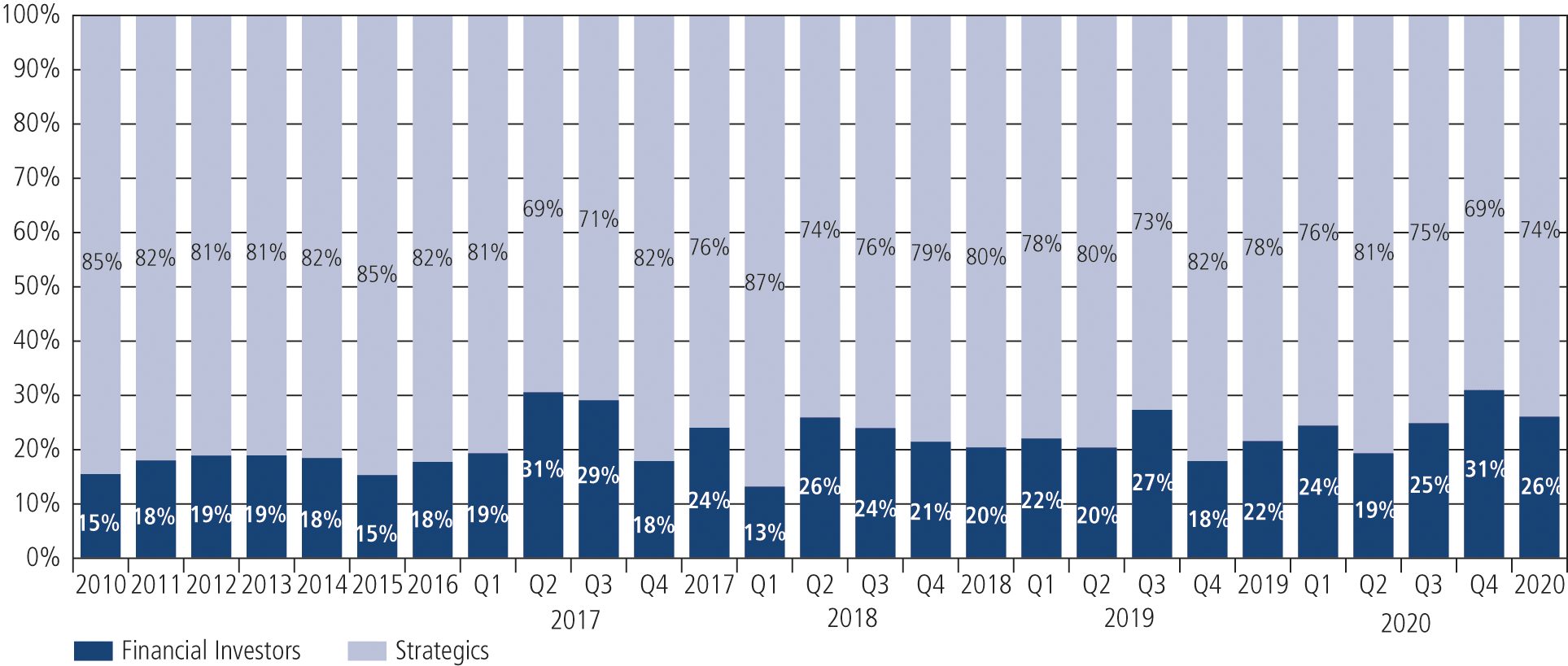

In the fourth quarter of 2020, the share of transactions with strategic investors fell by 6 percentage points compared to the previous quarter, from 75 per cent to 69 per cent. Compared to the same quarter last year, the share of transactions with strategic investors fell by 13 percentage points. For the year as a whole, the share of transactions with strategic investors was 74 per cent, which is below the average of 79 per cent over the last 10 years.

4. Outlook

After a strong third quarter, activity in the M&A market again increased significantly in the fourth quarter. The M&A market in the Americas in particular continued to recover, but was not quite able to make up for its losses in the first half of the year, while in Europe the strongest fourth quarter since the financial crisis was recorded. It was also observed that the cross-border transaction volume increased again as well as more transactions were announced in sectors that are directly or indirectly affected by the measures to combat the Corona pandemic. These could already be the first signs that companies are looking more confidently to the coming year.

Nevertheless, the number of new infections has increased significantly again worldwide and many countries in Europe have again imposed strict lockdowns with business closures and partial curfews to contain the spread of the virus. The duration of these renewed lockdowns and the impact on the economy are currently difficult to predict. However, with the results of the clinical trials and the approval of the first vaccines, there is now a light at the end of the tunnel.

In view of the economic challenges, it is to be expected that a large number of companies will examine the sale of peripheral activities in order to further focus the core business and strengthen the balance sheet, which has been weakened by Covid. This trend may also be driven by the return of activist investors. In addition, companies are under pressure to drive the digitisation of their business model and are therefore specifically looking for suitable acquisitions. As a result, the line between traditional companies and technology companies is becoming increasingly blurred. Financial investors continue to have high cash reserves that want to be invested profitably, while at the same time the current high company valuations offer a good opportunity to sell investments. Financing acquisitions is also not a problem in the current environment. Despite the existing uncertainties, there are many indications that an acceleration of M&A activity can be expected for the coming year.