Outlook for the German M&A market in 2026

1 Introduction

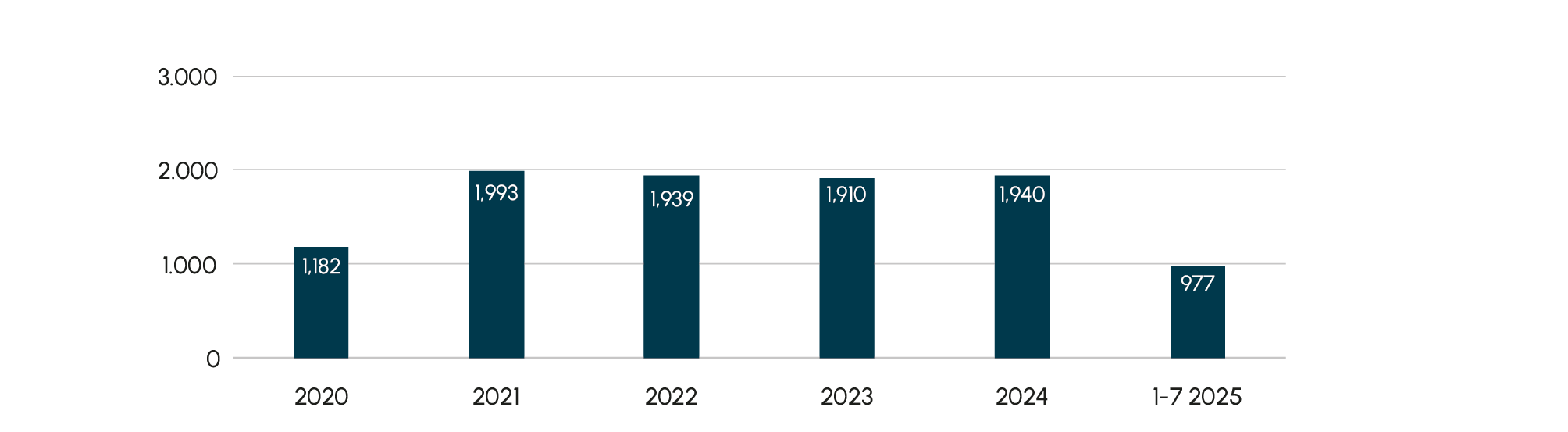

Poor economic forecasts, high energy costs, new US tarifs and the weakening US dollar relative to the euro are challenging conditions for M&A transactions in Germany. It is therefore hardly surprising that in the current year 2025 – similar to the previous three years – the number of deals in the mid- and large-segment has remained at a disappointing level. Despite the generally subdued sentiment, there are compelling reasons to believe that the market for mergers and acquisitions will recover significantly over the next 18 months.

In times of enormous economic and geopolitical uncertainties, it has become increasingly difficult to reach an agreement between buyers and sellers on company valuations when it comes to forward looking business plans. Corporates have also become cautious and are holding back on risky, large-scale acquisitions. As a result, according to Mergermarket, in the first seven months of this year only 957 German companies of a certain size changed ownership. During the comparable periods of 2023 and 2024, the respective number of deals totaled 1,119 and 1,108.

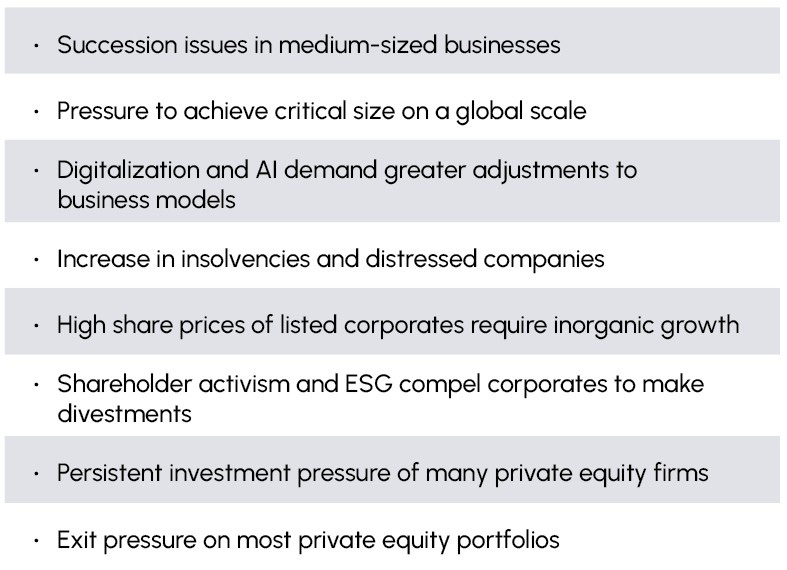

Nonetheless, there are still numerous drivers of mergers and acquisitions: Higher requirements for critical company size, succession issues in family businesses, and the growing relevance of digital business models and AI applications are pushing many medium-sized companies toward bold acquisition strategies or sales to larger or financially strong partners.

2 Investment pressure on the buy-side

The persistently high stock market valuations of publicly listed large corporations are prompting executives to actively consider acquisitions. In many cases, current valuations can only be sustainably justified if companies grow not only organically but also inorganically. At the same time, private equity investors are holding significant cash reserves, putting them under enormous pressure to find suitable acquisition candidates for the funds they have raised.

3 Resolution of an enormous exit backlog

Another key driver is the dal jam and thus M&A backlog caused by postponed succession solutions, private equity exits and corporate divestments over the past three years.

Looking at corporate succession planning, Germany’s medium-sized businesses face a massive exit wave. In the next two years, around 190,000 successions are expected – a figure that will increase to over 500,000 in the medium term due to demographic change. Succession issues will inevitably also lead to heightened sales activity in the midmarket. The need for larger corporate entities with global footprints is forcing many mid-sized Mittelstand companies to sell to a larger competitor or to a financially strong partner.

In addition, many private equity firms are under significant pressure from their investors to bring longstanding portfolio companies into exit transactions in order to generate cash flow returns. On average, portfolio companies have been getting older. When the market conditions aren’t yet favorable for a sale, continuation funds come into play. Examples of such transactions in Germany include vehicles formed by Triton, DBAG, DPE, and Oakley, which together have invested several billion euros.

Finally, German corporations are increasingly forced, under pressure from activist key shareholders, to consider divestments. As a result, many companies can no longer afford to indefinitely postpone portfolio optimizations. For example, Thyssenkrupp is planning a potential sale of its Materials Services division, which generates approximately EUR 12 billion in annual revenues and represents a significant part of the corporation.

4 Importance of ESG topics

In the coming years, ESG themes will continue to grow in importance across corporations, private equity firms, and financing banks. Compliance with environmental regulations, encouragement of diversity, and exemplary business practices are increasingly influencing acquisition and divestment decisions. Specifically, efforts around decarbonization and the broader energy transition will motivate companies to acquire environmentally friendly technologies and key competencies. M&A is becoming an increasingly critical management tool for improving ESG profiles.

5 M&A activities across nearly all industry sectors

With the share of transactions in non-cyclical sectors further increasing at the expense of cyclical industries. Above-average M&A activity is expected in areas such as software, artificial intelligence, digitization, infrastructure, renewable energies, technology, medical technology, and healthcare. Additionally, we anticipate a boost in M&A activity in sectors under increasing strain like retail and the weakening automotive supplier industry. Opportunities in these sectors arise through distressed M&A, turnarounds, or restructurings. On the other hand, we foresee a slowdown in M&A within machinery and plant engineering as well as the chemicals industry.

6 High proportion of cross-border deals

We anticipate that the share of cross-border deals will continue to rise in 2026, reaching approximately 75%. As in previous years, foreign buyers will acquire more German companies than vice versa. The most important buyer and target nation for German companies remains the U.S., followed by the UK and France. Purchase price multipliers are likely to face pressure due to the declining earnings dynamics of many companies. Furthermore, we expect a majority of transactions to take place in the so-called mid-cap segment, with large acquisitions such as Siemens’ recent $5 billion purchase of the U.S. software company Dotmatics remaining the exception.

7 Attractive times for sellers and buyers

For owners of profitable, healthy companies in particular, the window should be wide open in the coming 18 months for a successful company sale on attractive terms. However, strategic buyers and financial investors are increasingly more cautious in M&A transaction from year to year. In due diligence, they will continue to thoroughly examine the target companies for the existence of any risks and obligations. To hedge against risks, they will try to enforce extensive warranties and indemnities. W&I insurance will continue to gain importance, also if the seller is a private owner or a family business.

There will be increasing opportunities for buyers to find exciting targets in the Mittelstand at fair valuations. However, the German M&A market will remain fragile, as it has been for the past three years. Dealmakers will continue to live with higher uncertainty and navigate a challenging macroeconomic environment and business outlook. Buyers will need to be calculated and entrepreneurial if they want to make successful deals. They should be mindful of potential risks while looking for opportunities and preparing to quickly close a deal when the time is right. Experience shows that economic downturns ca be very rewarding times for deal hunting.

Conclusion

Due to the accumulation of delayed transactions, we expect mid-sized M&A activities to increase in 2026 by around 20% compared to 2025. Our deal pipeline and numerous discussions with major corporations, financial investors, family business owners, and financing banks support this outlook. As a result, we might see a total of around 2,400 M&A transactions involving a German target company. This positive outlook is also strongly reflected in the recent stock price developments of publicly listed M&A investment banks.