Potential pitfalls in W&I claims: A finance perspective

Introduction

Global M&A transactions reached a new all-time high in 2021. However, as a result of the war in Europe and Covid-19 disruptions, inflation and other market risks are increasing – as well as uncertainties in M&A transactions. Learn why an increasing number of companies are preparing for disputes following M&A deals, what advantages warranty & indemnity insurance can offer and what decision-makers should know.

A recent case

Sellers can face significant claims for damages if a financial statement warranty turns out to be false. A recent case in the aviation industry demonstrates how you can protect yourself against such claims. Shortly after signing the sale and purchase agreement (SPA), the buyer of an airline discovered lease agreements for two airplanes were accounted for incorrectly. The management of the airline had assumed that it was reasonably certain to exercise a renewal option on the lease. However, the lease agreement itself did not even contain such an option.

It was pretty obvious: the seller had breached a warranty. However, the buyer of the airline had entered into a warranty and indemnity (W&I) insurance policy, which covered the risk and protected the parties against the consequences. The buyer could claim the damages directly from the policy holder and – after negotiations behind closed doors – achieved a settlement of around EUR 8.5 million.1

W&I insurances in the current market environment

Recent market studies demonstrate a growing popularity of the involvement of W&I insurance in M&A deals last year. This development is not surprising since the global M&A activities in 2021 reached a new all-time high – both in the number of transactions and purchase prices2 – with deal value totaling USD 5.1 trillion.3 Based on our observations, this trend continued at least in the first half of the current year. As prices rise, so does the buyer’s need for protection.

As a consequence, the W&I business recovered rapidly after a drop-off in 2020 during the Covid-19 pandemic. Insurers even reached personnel capacity limits temporarily.4,5 The share of transactions involving such specialty insurance products rose to a record level of 19% in 2021 versus just 10% in 2010.

The bigger the deal, the higher the demand for M&A insurance. In almost half of transactions with a value of more than EUR 100 million, the parties made use of W&I policies.6

In our view, the portion of insured transactions will continue to rise. Despite the war in Ukraine and rising inflation and market risks, purchase prices remain high. In our experience, M&A disputes may become more frequent in the event of an economic downturn. If a downturn occurs between signing and closing, the negotiated price may appear subsequently inflated and a buyer may try to identify opportunities to reduce the purchase price or obtain compensation based on the SPA.

Significant advantages of W&I policies

W&I insurance facilitates the sale and purchase process and provides high strategic value to both sellers and buyers. Sell-side first: by means of an insurance, sellers can limit their liability and transfer the risk relating to breaches of warranties in a SPA to insurance companies, as shown in the case at the beginning of this article. The insurers, not the sellers, are then liable if a representation or warranty turns out to be false.

In this context, the insurance provides a clean exit from the investment. Thus, sellers can determine and distribute sales proceeds much earlier. As a result, W&I policies are an effective tool to close gaps and overcome transaction hurdles between the positions of buyers and sellers: they offer additional leeway in negotiations and can significantly accelerate the closing of transactions.

But buyers also benefit from the insurance coverage, particularly in situations where no solvent debtor is available or the seller is a special purpose entity (SPE). Based on our experience, enforcing claims against such debtors arising from breaches of representations and warranties is difficult if no W&I insurance exists. However, well-known insurance companies may provide sufficient credit ratings. Other protection mechanisms such as escrow accounts which (partly) delay the payout of the purchase price become redundant.

Another advantage of W&I policies is the relatively low premium costs in recent years: today, insurance premiums often amount to approximately one percent or less of the risk to be insured.7 At the same time, the insurable amounts have increased, and the insurance companies have invested in employees with a M&A background. Hence, the further professionalisation of both insurers and brokers enables them to provide tailored insurance solutions under challenging deadlines which offer a customer-oriented service approach.8

Typical types of W&I claims

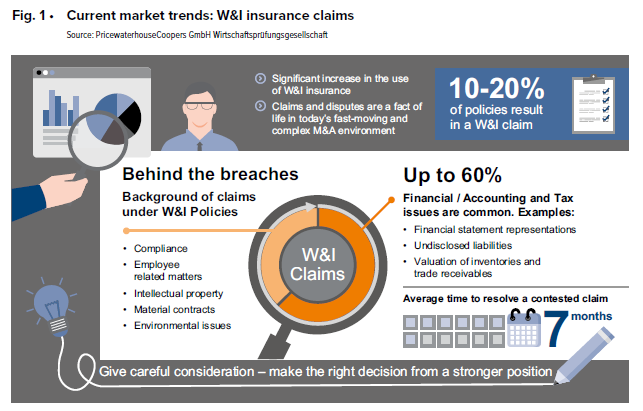

Our observations and current market studies show that between 10 and 20% of M&A transactions result in a W&I claim. The bigger the deal, the more claim notifications. In deals with a value of more than one billion US dollars, the share of claim notifications amounts to 21% per an AIG study.9

Insiders assume that this rate will continue to rise. In times of high purchase prices and a volatile market environment, buyers often analyse whether purchase price adjustment mechanisms, warranties or indemnification clauses offer opportunities for subsequent purchase price adjustments.

Given the extraordinarily high level of uncertainty in the current market environment, there is a high risk that geopolitical conflicts, supply chain disruptions or implications due to the Covid-19 pandemic will throw the buyers’ underlying valuations overboard – potentially even before closing of the transaction as several weeks or even months often pass between signing and closing. In those cases, special consideration is drawn to price adjustment clauses or comparable mechanisms – which are included in about half of all SPAs.

Disappointed investors often intuitively put their spotlight on financial statements and other financial information, as well as tax-related issues. According to recent market studies, about half of all W&I claims relate to this category and are the key driver for W&I claim notifications.10

This is not surprising, as financial data are the basis for common valuation models and consequently for determining the purchase price. Accordingly, buyers usually request additional assurance from sellers that the financial information have been prepared in accordance with applicable generally accepted accounting principles and/or present a true and fair view on the assets, liabilities, operations and cash flows (financial statements warranty). Therefore, sellers may face significant recourse if they violate agreed accounting principles. If a buyer subsequently identifies material misstatements such as the erroneous lease accounting in the example described at the beginning, sellers should expect significant damage claims.

Other common drivers of W&I claims are breaches relating to material contracts, intellectual property, compliance issues, employee-related matters and environmental issues.11

Identification and enforcement of claims

In W&I claims, the parties usually argue about multi-million dollar issues. In order to identify and successfully enforce contractual claims, a systematic approach, comprehensive expertise regarding financial and legal related issues and in-depth experience in handling the claims are therefore essential.

The main challenge in identifying claims is that they are rarely unambiguous or indisputable. On the contrary, W&I claims are often based on financial information underlying complex accounting principles or contract-specific regulations.

These regulations often require significant management judgment for example in accounting estimates. Conflicts between sellers and buyers therefore regularly arise from subjectivity, which is unavoidable in applying recognition and measurement criteria in accounting.

Once buyers have identified claims, it isn’t sufficient to simply report those damages to the insurance company. Instead, it is required to systematically analyse the legal and economic basis for a claim and to prepare financial data and other relevant facts in detail.

In-depth analysis and mindful communication

Buyers should intensively consider opportunities and risks. To do so, decision-makers must analyze the probabilities of success - taking into account the fact that it may cost time and money to enforce a W&I claim. With an average settlement period of seven months, which can also be significantly exceeded, no one should underestimate this aspect.

In case potential claims arise from breaches of representations and warranties, it is important to gather all relevant facts and circumstances, analyze the financial data, identify the relevant issues and work out the economic implications. Each SPA as well as the W&I policy is a customized solution tailored to meet the specific needs of a transaction. The underlying factors and intentions are necessary to assess whether an issue is covered by the insurance or not.

Involvement of dedicated experts is crucial for the outcome of a W&I claim. Based on their extensive transaction and claim experience they can estimate a reliable range of the potential settlement amount and respective success rates. This forms the basis to reach a favorable result during negotiations. However, they also support policyholders or insurers in investigating, processing and presenting potential claims.

Precise and proactive communication and reporting are extremely important in this context. Reports and statements must be clearly structured. In addition, convincing arguments must be drafted, supported by substantial evidence. This significantly increases the chances for a successful claim and at the same time builds the grounds for a trustful long-term business relationship between customer and insurance company.

1 Howden M&A (2022): Claims Report 2021. In: https://howdenmergers.com/documents/downloads/6296%20M&A%20Claims%20report%202021%20v14.pdf (abgerufen am 20.05.2022), p. 19. 2 PwC(2022: Global M&A Industry Trends 2022. In: https://www.pwc.com/gx/en/services/deals/trends.html (abgerufen 20.05.2021), p.1. 3 Referring to publicly disclosed deal values. 4 AIG (2022): M&A Claims Intelligence report. In: https://www.aig.com/business/insurance/mergers-and-acquisitions/mergers-and-acquisitions-claims-reports (abgerufen am 20.05.2022), p. 2. 5 Zusammenhang mit M&A Transaktionen. In: Der Betrieb, Beilage 03, Heft Nr. 51-52, p. 31. 6 CMS (2022): CMS European M&A Study 2022. In: https://cms.law/en/deu/publication/cms-european-m-a-study-2022 (abgerufen am 20.05.2022), p. 57. 7 Haßler/Daghles (2016): Warranty & Indemnity-Insurances im M&A-Markt – ein Überblick. In: https://blog.handelsblatt.com/rechtsboard/2016/10/17/warranty-indemnity-insurances-im-ma-markt-ein-ueberblick/ (abgerufen am 20.05.2022), p. 4. 8 Haßler/Daghles (2016): Warranty & Indemnity-Insurances im M&A-Markt – ein Überblick. In: https://blog.handelsblatt.com/rechtsboard/2016/10/17/warranty-indemnity-insurances-im-ma-markt-ein-ueberblick/ (abgerufen am 20.05.2022), p. 4. 9 AIG (2021): M&A Claims Intelligence report. In: https://www.aig.com/content/dam/aig/america-canada/us/documents/business/management-liability/aig-manda-2021-w-and-i.pdf (abgerufen am 20.05.2022), p. 3. 10 Liberty GTS (2021): 2021 claims briefing – Exclusive insights guiding global decision-making. In: https://www.libertygts.com/static/2021-09/GTS_ClaimsBriefing_2021FINAL+%281%29_0.pdf (abgerufen am 20.05.2022), p. 17. 11 AIG (2021): M&A Claims Intelligence report: In: https://www.aig.com/content/dam/aig/america-canada/us/documents/business/management-liability/aig-manda-2021-w-and-i.pdf (abgerufen am 20.05.2022), p. 3.